July 10, 2026 · By WingCore Editorial

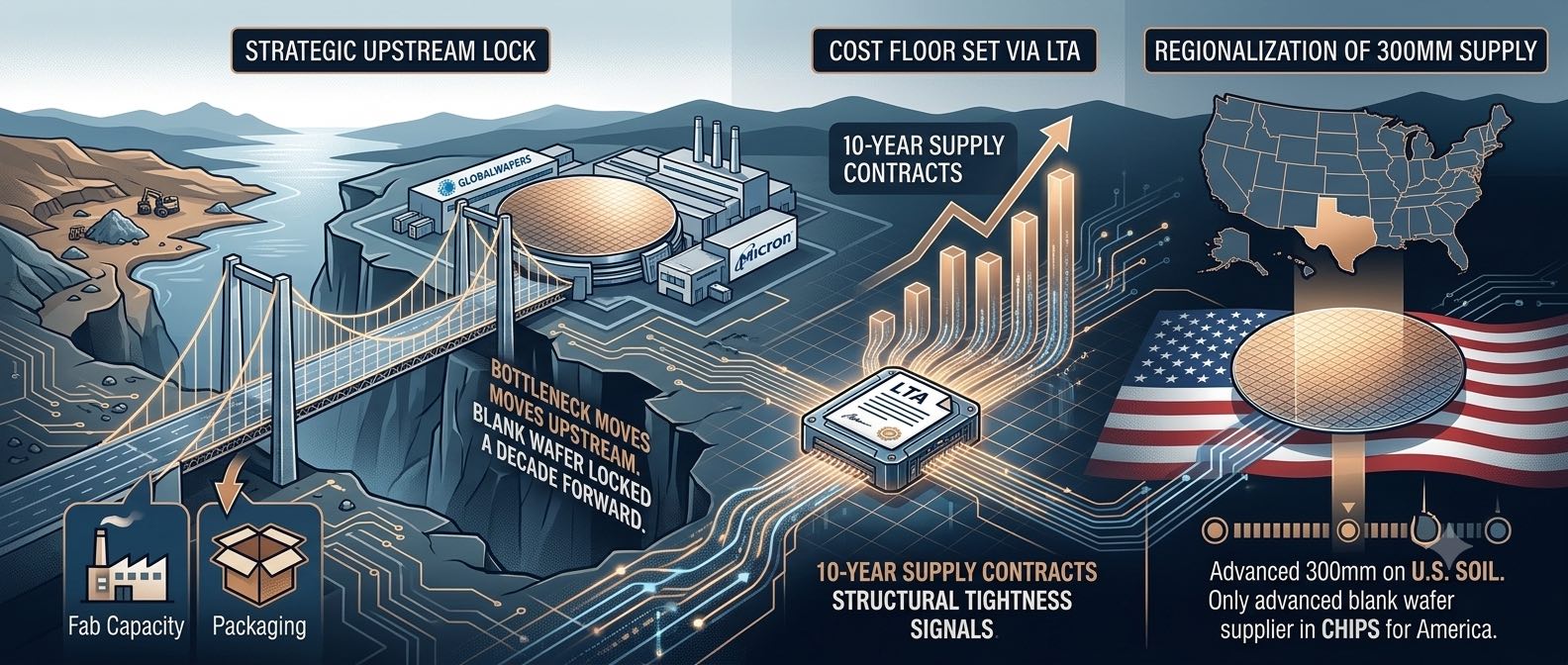

When a Memory Maker Locks a Decade of Raw Wafers: What Micron's $3B GlobalWafers Move Signals for OEM and EMS Sourcing Strategy Through 2027

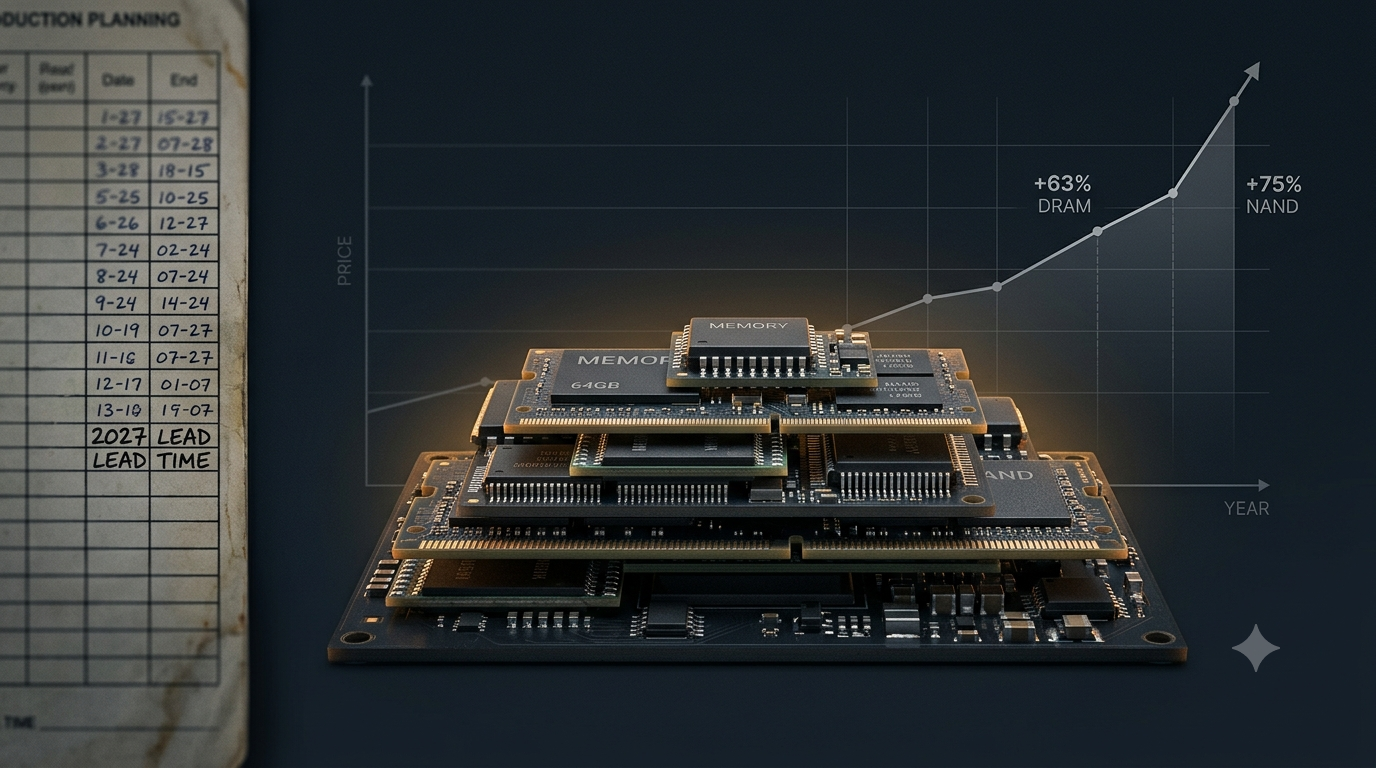

Micron's July 9 announcement — up to $3 billion to strengthen the U.S. semiconductor ecosystem, $500M in strategic financing for GlobalWafers' Sherman, Texas 300mm plant, and a ten-year raw silicon wafer supply agreement — is being read by markets as a stock story. For sourcing organizations, the more durable signal sits one layer higher in the chain: the bottleneck is migrating from fab capacity to substrate supply, and it is being regionalized.

Read more →