The Next HBM-Style Squeeze Is in Passives: Why AI-Server MLCC Demand Is Crowding Out General-Purpose Capacitors and Reshaping OEM and EMS Sourcing

The component market has spent two years watching AI accelerators vacuum up HBM and DRAM capacity. The same dynamic is now playing out in multilayer ceramic capacitors, where a single AI rack can consume nearly nine times the MLCCs of a traditional server. The consequence for OEM and EMS buyers is not just higher prices on premium parts — it is the quiet erosion of allocation for the general-purpose and industrial MLCCs that fill ordinary bills of materials. This piece examines what that means for sourcing strategy through the second half of 2026.

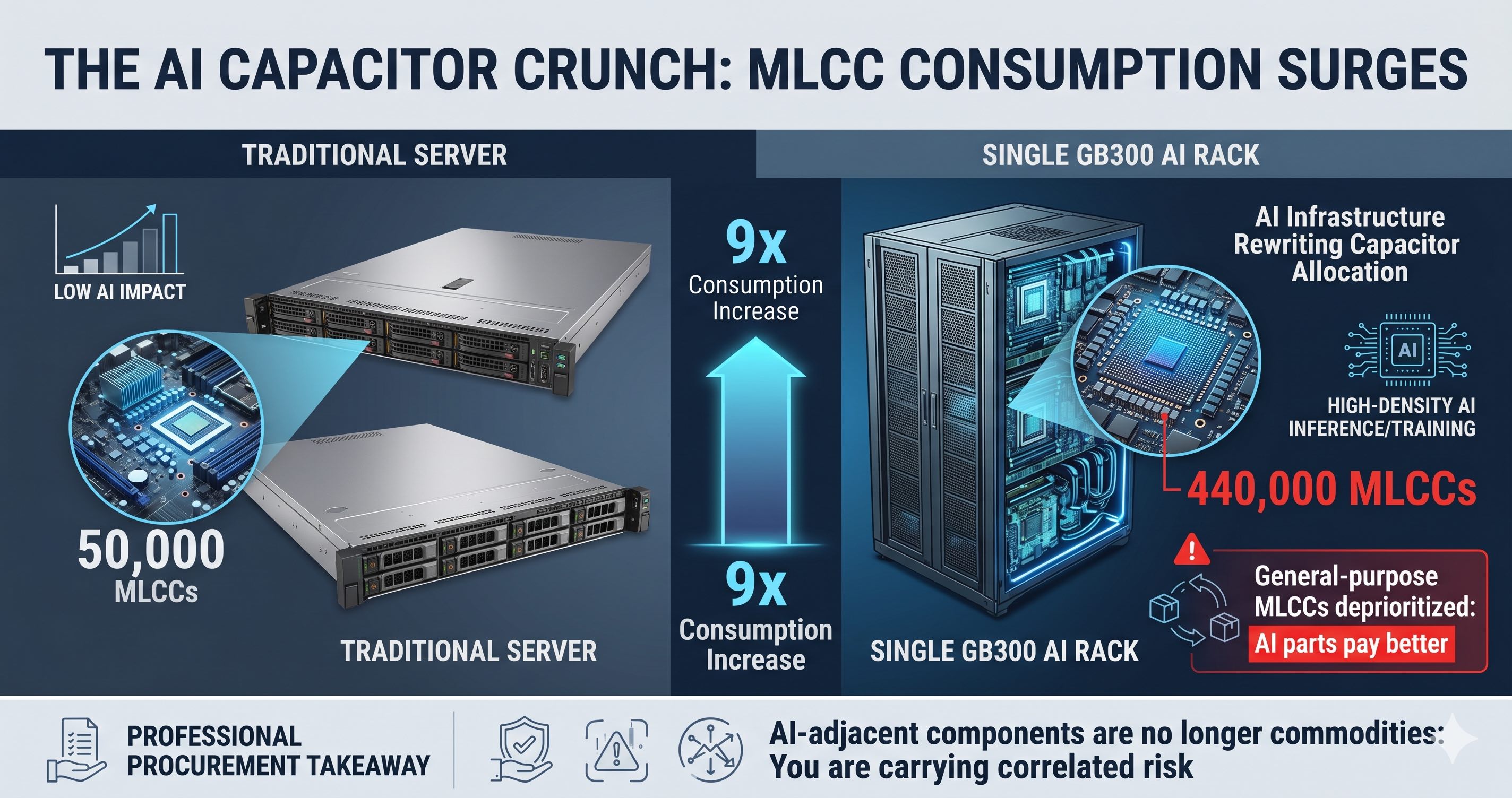

For most of the past two years, the defining supply story in electronics has been memory. High-bandwidth memory and DDR5 capacity were pulled toward AI accelerators, contract prices climbed quarter after quarter, and procurement teams learned to treat memory as a strategic, allocation-controlled commodity rather than a catalog purchase. That lesson is now migrating to a component category that buyers have historically treated as background noise: the multilayer ceramic capacitor.

The scale of the shift is easiest to grasp through a single comparison. A conventional server consumes on the order of fifty thousand MLCCs across its boards. A current-generation AI rack built around NVIDIA's GB300 silicon requires roughly four hundred and forty thousand — close to nine times as many. Those capacitors are not exotic specialty parts; they are the small, high-capacitance, high-voltage devices used for power filtering, decoupling, and signal integrity around dense GPU and memory clusters. As hyperscalers and system integrators race to stand up AI infrastructure, that per-rack content explosion translates directly into enormous incremental demand on a finite production base.

The three dominant suppliers — Murata, Taiyo Yuden, and Samsung Electro-Mechanics — have responded the way any rational manufacturer would. They are routing capacity toward the high-capacitance, high-voltage parts that carry the best margins, which in practice means AI-server and premium automotive grades. Lead times on those parts have already stretched from the eight-to-twelve-week range into sixteen to twenty-four weeks, and some specifications are now subject to order restrictions. The April price actions, in which the leading makers raised prices across portfolios by fifteen to thirty-five percent, were an early and visible signal. But for buyers, the price line is the part of the story that is easiest to plan around. The harder problem is allocation.

Here is the mechanism that matters for sourcing teams. Because MLCC capacity is fixed in the short term, every wafer of production redirected toward AI-server parts is a wafer not available for the general-purpose, consumer, and mid-range automotive capacitors that populate ordinary industrial and commercial designs. The Big Three are not short of the technology to make those general parts; they are simply deprioritizing them. Unmet general-purpose demand is therefore spilling outward — first to second-tier Taiwanese makers such as Walsin and to Yageo's secondary lines, and from there into the broader spot and secondary channel, where prices have already risen fifteen to twenty percent. A buyer who assumed their commodity MLCCs would always be available on short lead times is discovering that the assumption no longer holds, even though no maker has formally declared those parts on allocation.

The strategic implications run in two directions. For OEMs and EMS providers whose products depend heavily on general-purpose and industrial MLCCs — power supplies, motor drives, energy-storage systems, EV charging hardware, industrial control — the prudent move is to treat these parts the way memory has been treated since 2024. That means extending forecast horizons, locking third-quarter and fourth-quarter requirements early rather than buying reactively, and qualifying second sources before the primary maker's lead time forces the decision. A design team that specifies a part today still has room to maneuver; a buyer who waits until the line is down does not. The cost of carrying a few extra weeks of general-purpose MLCC inventory is trivial next to the cost of an AI-adjacent shortage cascading into an unrelated industrial build.

The second implication concerns risk. As volume shifts into the secondary and spot channel, the exposure to counterfeit, remarked, and refurbished parts rises sharply — and passives are a notoriously difficult category to authenticate, because the parts are tiny, unmarked at the package level, and easy to mix across date codes. Buyers who are forced into the spot channel for general-purpose MLCCs should insist on date-code traceability and source from partners who can document chain of custody, rather than chasing the lowest spot quote. The discipline that procurement organizations applied to memory authentication over the past two years needs to extend to passives now.

There is a broader read here for anyone planning component strategy into 2027. The AI build-out does not constrain only the components it directly consumes; it constrains everything that shares a production base with them. Memory was the first category to demonstrate this, power semiconductors followed, and passives are now showing the same pattern. The capacitor squeeze is unlikely to resolve before the middle of 2027 on current capacity timelines. The OEM and EMS organizations that come through it cleanly will be the ones that stopped treating any AI-adjacent component as a commodity and started treating the entire shared-capacity supply base as a single, correlated risk.