Helium Becomes the Quiet Single Point of Failure in the 2026 Memory Supply Chain — A Sourcing Read for OEM and EMS Buyers

The 2026 memory squeeze has been told almost entirely as a pricing and allocation story. This week reframed it as a raw-material risk. A strike on Qatar's Ras Laffan halted helium output, doubled spot prices, and forced Korean memory fabs to ration a gas with no substitute. For OEM and EMS procurement, helium concentration risk is now a line item that deserves the same attention as wafer allocation.

The 2026 memory shortage has, for nearly a year, been narrated through one lens: pricing. Contract resets, allocation lockouts, double-digit quarterly jumps. That framing is accurate but incomplete, and this week exposed the gap. The most consequential development was not another price sheet — it was a gas most buyers have never had to think about, and a supply geography that turns out to be alarmingly concentrated.

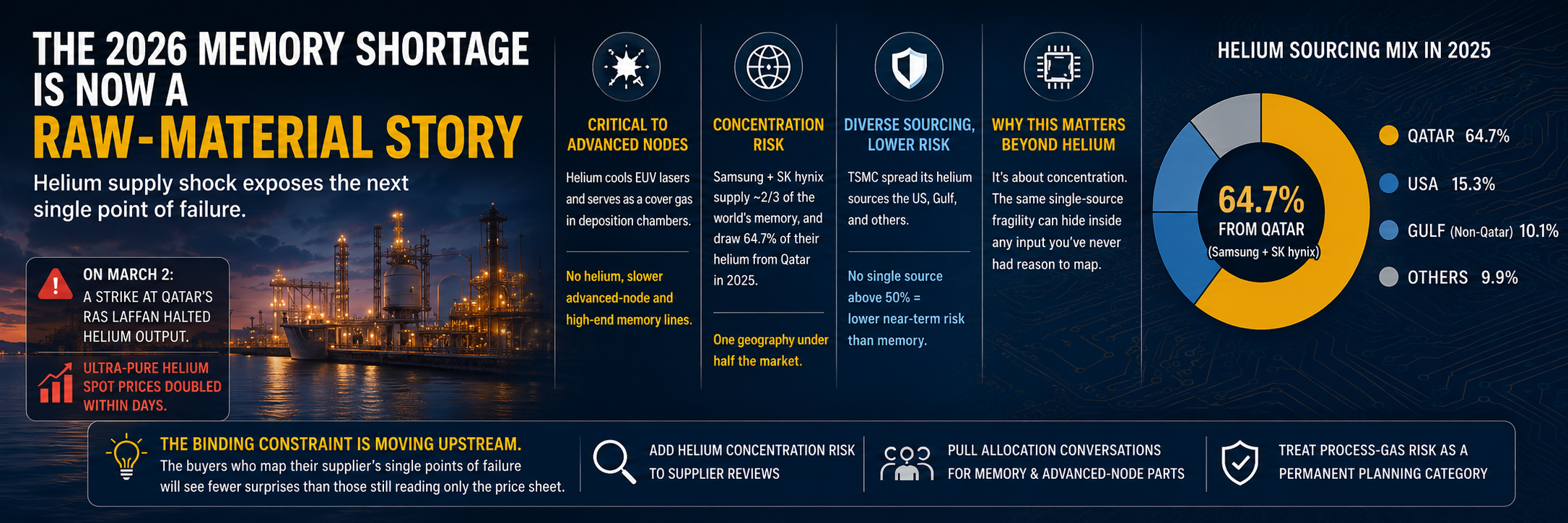

On March 2, Iranian drones struck Qatar's Ras Laffan Industrial City, one of the world's largest hubs for liquefied natural gas and the helium that comes with it. QatarEnergy briefly halted LNG and associated helium production, helium movements through the Strait of Hormuz stalled, and within days the consequences reached the cleanrooms of South Korea. Ultra-pure helium spot prices doubled, and fabs began rationing. For a material with no functional substitute, rationing is not a minor inconvenience — it is a direct constraint on output.

Helium's role in advanced manufacturing is easy to underestimate precisely because it is invisible in a bill of materials. It cools the lasers in EUV lithography systems and acts as a cover gas in the deposition chambers that build the metal interconnect layers inside every advanced logic and memory die. When helium tightens, cycle times stretch, yields come under pressure, and the most advanced, most helium-intensive processes feel it first. This is not a cost-of-goods nuisance; it is a throughput question at the leading edge.

The exposure is profoundly uneven, and the asymmetry is the part procurement teams should internalize. Samsung and SK hynix together supply roughly two-thirds of the world's memory, and in 2025 those two companies drew 64.7% of their helium from Qatar. A single sourcing geography therefore sits underneath half the global memory market. TSMC, by contrast, deliberately spread its helium procurement across at least three non-correlated geographies — the United States, Gulf producers, and others — with no single source accounting for a majority of volume. That sourcing discipline is why, faced with the same shock, logic faces materially lower near-term risk than memory. The lesson is not about helium specifically; it is about concentration. The same single-source fragility can hide inside any input a buyer has never had reason to map.

For OEM and EMS procurement, the practical implications follow directly. First, helium concentration risk should be added to supplier risk reviews as an explicit factor, particularly for memory-heavy bills of materials, because the upstream exposure of your memory supplier is now part of your own risk profile whether or not you can see it. Second, parts whose production is helium-sensitive — DRAM, DDR5, enterprise NAND and SSD, HBM, and leading-edge logic — warrant earlier allocation conversations and longer planning horizons, since recovery from a geopolitical disruption of this kind is measured in months, not days. Third, this episode argues for treating raw-material and process-gas risk as a permanent category in supply planning rather than a one-off headline; helium today, a specialty gas or substrate tomorrow, the structural lesson is identical.

It is also worth separating signal from noise. On June 5, AMD and Intel led a broad semiconductor sell-off, amplified by a cautious AI outlook from Broadcom and ongoing memory-shortage sentiment. Equity volatility of that kind reflects positioning and sentiment; it does not reflect any easing in the physical supply picture, which remains tight across memory, advanced packaging, and now the upstream gases that feed both. Reading a share-price pullback as a fundamentals reversal would be a mistake.

The broader point is a shift in where the binding constraint sits. For most of this cycle, the question was how much memory would cost and who would get allocation. The helium episode moves part of that question upstream, into the raw materials and process inputs that determine whether the wafers can be made at all. Buyers who map that layer — who know not just their supplier, but their supplier's single points of failure — will navigate 2026 with fewer surprises than those still reading only the price sheet.