From Pricing Cycle to Allocation Reality: How Kioxia's 2026 Sell-Out, 332-Layer QLC, and 245TB SSDs Reshape Industrial and AI Storage Procurement

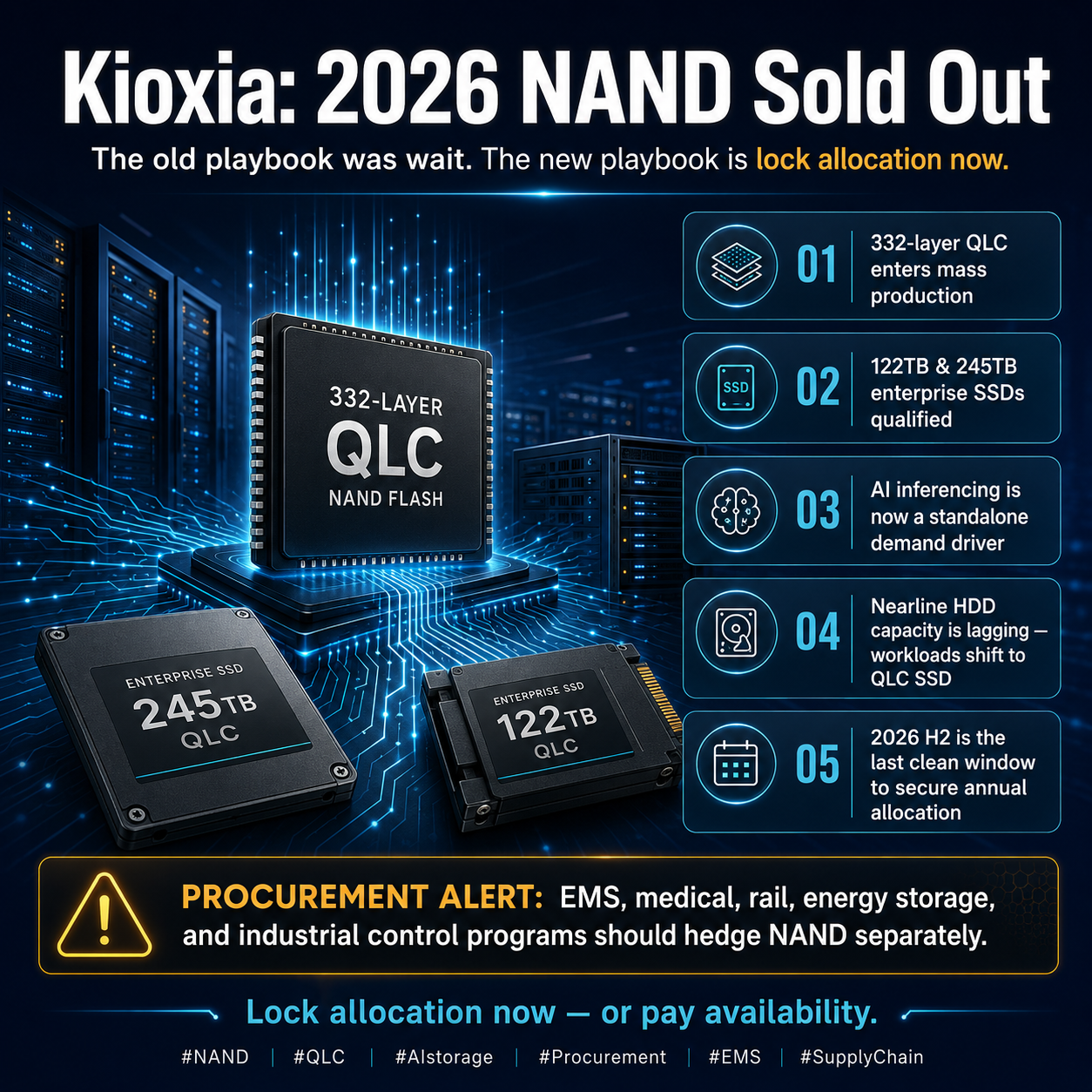

Kioxia's public acknowledgment that calendar 2026 NAND production is fully allocated is not just another supply headline. Combined with the 332-layer QLC ramp and the qualification of 122TB and 245TB enterprise SSDs, it signals a structural shift in how the storage tier will be built for AI inferencing and how nearline HDD workloads migrate to SSD. Industrial OEMs and EMS buyers should treat 2026 H2 as the last clean planning window before allocation becomes the dominant scarcity, not price.

For most of the past decade, the working model in NAND procurement has been a pricing cycle. Inventory levels rise and fall, contract pricing follows roughly six months behind, and most professional buyers learn to time orders against that rhythm. The cycle absorbed cyclical demand from smartphones, PCs, and the first generation of cloud storage, and most procurement teams could plan a three-quarter horizon with confidence that any tightness would eventually resolve into a softer market.

That working model is now under serious pressure. Kioxia's memory business managing director recently stated publicly that the company's calendar 2026 NAND production is sold out, that the company can no longer adjust delivery dates and quantities against customer demand on a transactional basis, and that allocation is now being committed to long-term partners through annual supply plans that resemble "gentleman's agreements" more than purchase orders. Tight conditions are expected to extend into 2027, and even longstanding Kioxia customers are absorbing year-on-year price increases in the range of 30 percent. The pricing data is in line with the demand commentary across the rest of the supply chain.

What makes this announcement different from prior NAND tightening narratives is the specific composition of the demand that is driving it. Kioxia cites three converging factors. First, the traditional enterprise server replacement cycle continues, providing a baseline of incremental demand. Second, AI inferencing — not training — is now a discrete and growing buyer of high-capacity NAND. Third, the nearline HDD segment has not meaningfully expanded capacity, and workloads that previously sat on nearline HDD are migrating to high-capacity QLC SSDs. The first two are well understood. The third is the most underestimated element in the 2026 storage outlook, and it is the one that determines whether this cycle behaves like prior NAND inventory cycles or whether it represents a structural reset.

On the supply side, Kioxia has been preparing for that shift. The company has publicly shown 332-layer process technology and shipped 122TB and 245TB QLC enterprise SSDs for customer qualification at the end of calendar 2025, with mass production scheduled to begin during this fiscal year. The density math is straightforward and significant. A single drive at 245TB allows a standard 2U server with 24 drive bays to deliver approximately 5 petabytes of raw capacity per chassis, before considering data reduction or RAID overhead. That density is exactly what AI inferencing data lakes have required and what nearline HDD has structurally been unable to provide at the latency profile that modern inference pipelines assume.

The procurement implications for industrial OEMs, EMS buyers, and integrated storage platforms are concrete. First, enterprise SSD spot pricing — particularly QLC at 8TB and above — is not expected to retrace toward 2024 lows during calendar 2026. Buyers should plan budget guidance and customer pricing on the basis that 30 percent year-on-year increases are now baseline rather than peak. Second, small-capacity eMMC and industrial SSD components, which have historically sat in the same fab loading queue as enterprise QLC SKUs, will continue to be deprioritized as QLC density ramps. Long-lifecycle industrial programs with small NAND content per BOM are likely to see longer lead times and tightening allocation, not because demand for those parts has spiked but because supply is being directed to higher-margin enterprise QLC.

Third, long-lifecycle programs in medical, rail, energy storage, and industrial control segments should now treat NAND as a separately hedged BOM line. Safety stock targets should be reviewed against a 6-month forward window, contractual price terms should ringfence NAND independent of general MOQ pricing, and second-source qualification should be accelerated for SKUs that have historically been sole-sourced. Fourth, secondary-channel sourcing — particularly 7.68TB and 15.36TB enterprise SSDs — should be monitored closely. These two SKUs are the most likely to be absorbed by server OEMs as allocation gaps open during 2026 H2, and the spread between primary and secondary channels is likely to narrow rather than widen as that absorption proceeds.

For EMS customers building platforms that today specify nearline HDD storage tiers, the window to redesign 2026 H2 platforms around high-capacity QLC SSD is closing. The economic comparison between nearline HDD and 245TB QLC SSD at the workload level is shifting more rapidly than most platform roadmaps assumed, and platform RFPs released into H2 2026 without an SSD-centric option are likely to be uncompetitive on both density and energy. Procurement organizations should be coordinating early with platform engineering to ensure that the SKU mix being qualified into 2027 designs reflects the supply reality, not the 2024 cost stack.

The strategic conclusion is the one that previous NAND cycles never required buyers to internalize. When a tier-one supplier publicly states that its annual production is sold out, the operating message to every buyer is that structural demand has overtaken the capacity that can be added on cycle time. Once AI inferencing demand and nearline HDD displacement close the loop, QLC NAND in enterprise storage starts to behave the way HBM behaves in AI training: the question is no longer the price, the question is whether the part is available. For industrial OEMs and EMS buyers, the 2026 H2 procurement window is the last clean opportunity to lock allocation, sequence design changes, and structure inventory before that shift becomes the dominant operating constraint.