The Nexperia Discrete Disruption Is a Structural Lesson, Not a One-Off: What OEM and EMS Buyers Should Institutionalize Before the Next Single-Node Failure

Nexperia's supply disruption has dragged from late September 2025 into mid-2026, with some legacy parts now quoted as unavailable until July 2026 or later. The headline is automotive pain, but the deeper lesson is structural: a single geopolitically exposed assembly-and-test node can sever a billion-dollar discrete supply with no warning. This is a strategic read for OEM and EMS sourcing teams on how to harden BOMs against single-node failure.

The Nexperia disruption has now outlasted most of the supply shocks that competed with it for attention over the past year, and that longevity is the point. What began in late September 2025, when the Dutch government took control of Nexperia's Netherlands-based operations and Beijing responded by halting exports from the company's Dongguan assembly-and-test facility, has not resolved into a clean before-and-after. As of mid-2026, customers holding higher-risk legacy positions are being told that new material may not be available until July 2026 or later, and several automakers are building their 2026 production plans on the explicit assumption that Nexperia supply remains volatile for months yet. A disruption that endures past three quarters is no longer an incident to be weathered; it is a structural feature of the supply base that procurement organizations must design around.

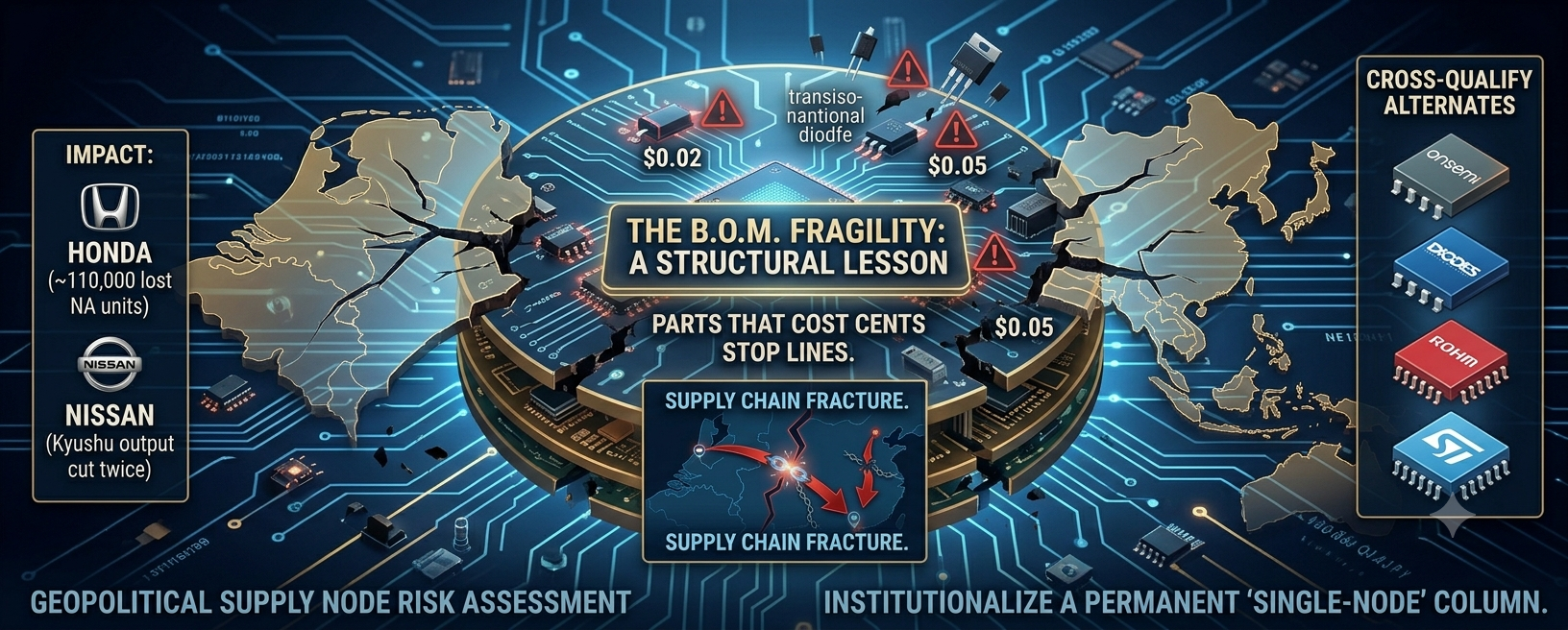

It is worth being precise about why a company most buyers rarely think about can rattle global automotive output. Nexperia generates roughly US$2 billion in annual revenue, with approximately 60% of its output sold into the automotive market, and its catalogue is dominated not by complex system-on-chip silicon but by the humblest layer of the bill of materials: logic gates, small-signal diodes and transistors, ESD protection devices, and MOSFETs. These are parts that cost a few cents each, populate a board by the dozen or the hundred, and carry an asymmetric risk profile — individually trivial, collectively indispensable, and capable of halting an entire assembly line when a single reference goes unfilled. Honda has pointed to roughly 110,000 lost North American units and an impact near ¥150 billion; Nissan trimmed output at its Kyushu plant twice in November 2025. The damage did not come from a scarce, high-value component. It came from the cheapest parts on the board, made unobtainable by a process bottleneck thousands of miles from where the cars are built.

That distinction is where the strategic lesson lives. The Nexperia shortfall is not fundamentally a capacity problem, and treating it as one leads buyers to the wrong remedies. The constraint sits at a single process step — back-end assembly and test concentrated at one site in a geopolitically contested jurisdiction — and no amount of front-end wafer availability resolves a back-end export halt. For OEM and EMS organizations, the implication is uncomfortable but clarifying: the resilience of a discrete supply line is determined less by the nominal number of suppliers and more by the geographic and political concentration of the steps those suppliers depend on. A part can be dual-sourced on paper and still be single-node in practice if both sources route through the same exposed back-end geography.

The near-term response is operational and should already be underway. Buyers need to scrub their BOMs specifically for Nexperia content, prioritizing not the highest-volume lines but the sole-source, old-package, low-usage positions that are most likely to disappear mid-build and least likely to be re-spun in time. Pin-to-pin equivalents from onsemi, Diodes Incorporated, Rohm, and ST should be qualified and written into the approved vendor list ahead of the gap rather than after it, while semi-compatible alternatives that require board changes need engineering evaluation queued now. Where a position is genuinely unique and cannot be changed, last-time-buy economics should govern coverage across the remaining lifecycle. Throughout, buyers should hold realistic expectations of the alternates: the manufacturers absorbing this redirected demand do not have unlimited capacity, and their lead times are stretching as Nexperia volume lands on them, which makes early engagement and early allocation materially more valuable than late spot pursuit.

The longer-term response is what separates organizations that merely survive this episode from those that are harder to disrupt next time. Single-node exposure deserves a permanent column in BOM risk assessment, distinct from supplier count, capturing whether a part's critical process steps concentrate in one politically exposed jurisdiction. Cross-qualification of alternates should be treated as standing infrastructure for critical discrete positions rather than an emergency measure invoked once the line is already down. And the secondary market, which will inevitably fill with these parts within days of any shortage, must be approached with discipline proportional to the elevated refurbishment, mixed-lot, and remarking risk that small-signal discretes carry relative to large silicon — channel provenance, original packaging, and date-code consistency verified, and small-lot qualification completed before any large commitment or non-cancellable order. None of these measures is novel. What the Nexperia disruption supplies is the unambiguous, costly proof that they are no longer optional. Today the exposed node belongs to Nexperia; the discipline worth institutionalizing is the assumption that tomorrow it belongs to someone else.