When the HBM Leader Lists in the US: What SK hynix's July 10 Nasdaq Debut Means for OEM and EMS Memory Sourcing Strategy Through 2027

SK hynix's July 10 Nasdaq ADR listing, arriving days after Samsung's July 7 Q2 preliminary print, binds the dominant memory supplier's capacity pricing to the public markets. For OEM and EMS procurement leaders, the event is less a finance milestone than a structural signal about how allocation, contracting discipline and pricing power will behave through 2027. This briefing reads the move for sourcing strategy rather than for shareholders.

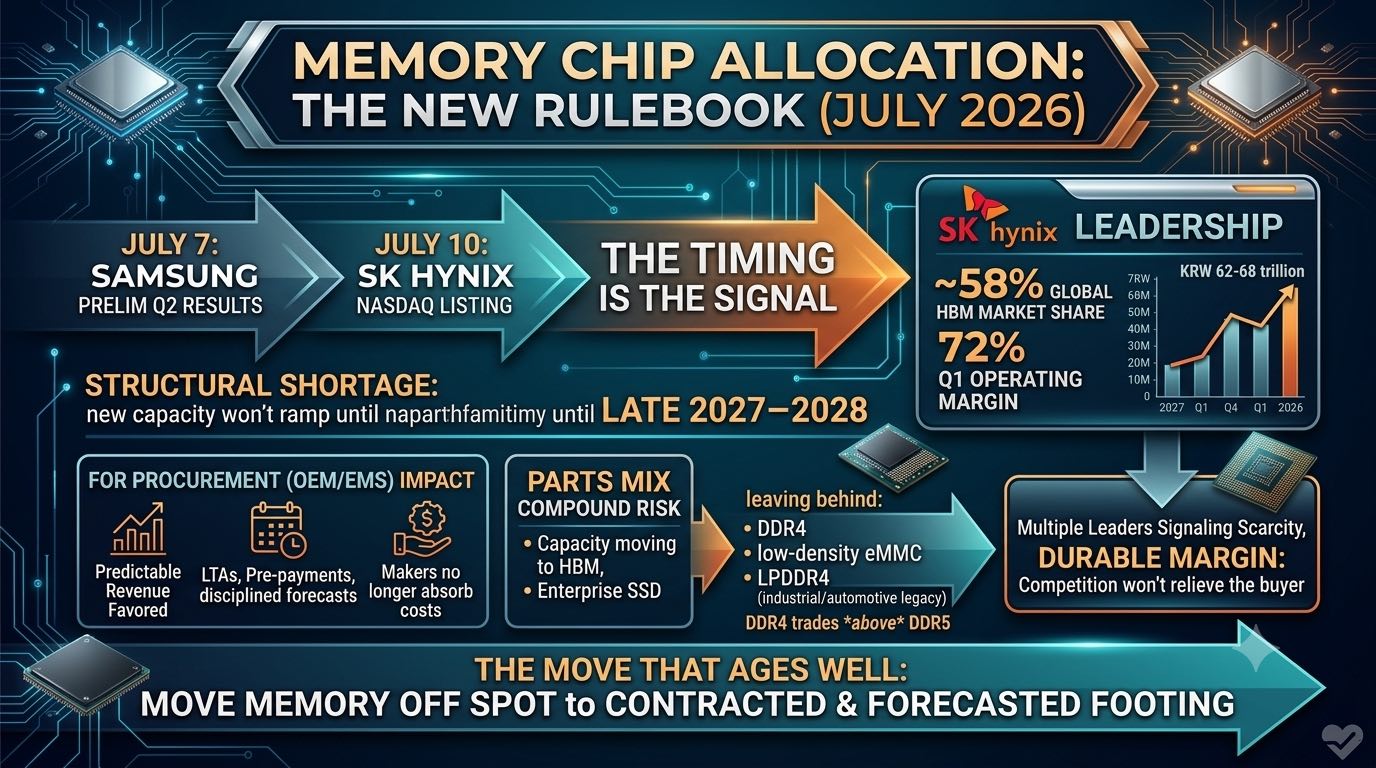

The scheduling tells you most of the story. SK hynix lists ADRs on Nasdaq on July 10, three days after Samsung releases its Q2 preliminary results on July 7. A company with roughly 58% of the global HBM market, a 72% Q1 operating margin, and a Q2 operating-profit consensus in the KRW 62-68 trillion range is choosing the peak of an AI memory cycle to broaden its capital base in the United States. Procurement teams should treat that choice as information, not noise.

A public listing does one thing above all: it capitalizes a forward view of capacity and pricing. For a memory leader in a structural shortage, that forward view is unambiguous — demand tied to AI infrastructure runs ahead of supply, new fab capacity will not ramp in volume before late 2027 or 2028, and the supplier intends to convert that scarcity into durable margin. The listing is a public commitment to defend pricing power rather than to chase share by discounting. For a buyer, that is the single most important read: the era of the memory maker absorbing cost to keep OEMs comfortable is over for the duration of this cycle.

That has direct consequences for how allocation is awarded. When a supplier is optimizing for margin and capital-market credibility, it rewards the customers who make its revenue predictable — those who sign multi-quarter long-term agreements, pre-pay or deposit against capacity, and provide disciplined full-year forecasts. Opportunistic, purchase-order-by-purchase-order demand becomes the residual that gets served last and priced highest. OEM and EMS teams that still run memory as a spot-managed line item are, in effect, volunteering for the back of the queue. The strategic response is to move as much memory demand as possible onto contracted, forecasted footing before the H2 allocation round closes.

The parts mix compounds the pressure. Capacity flowing toward HBM and enterprise SSD is capacity leaving conventional and legacy densities. DDR4, low-density eMMC and LPDDR4/LPDDR4X — the parts embedded in industrial, automotive and long-lifecycle designs — are being squeezed hardest, to the point that DDR4 now trades above DDR5 in an inverted market. For product lines with ten-year service commitments, this is the moment to formalize last-time-buy quantities and qualify alternates, rather than assuming the mainstream roadmap will carry legacy support.

Samsung's July 7 print should be read alongside the listing, not separately. The number that matters is not headline revenue but the HBM3E/HBM4E supply guidance and any commentary on conventional DRAM and enterprise NAND allocation. Two of the three dominant suppliers signaling the same posture — tight supply, disciplined pricing, allocation to committed customers — removes any expectation that competition between them will relieve the buyer. When both leaders read from the same script, the sourcing basis for H2 and into 2027 should be set conservatively.

The practical program for a procurement organization is straightforward to state and demanding to execute. Convert memory from a spot line into a contracted, forecasted category with named LTAs for HBM-adjacent and mainstream DRAM. Formalize last-time-buy and alternate-qualification plans for every legacy density in the BOM. Re-baseline standard cost and quoting assumptions above current spot, and hold that basis through the next two quarters. And read the July 7 and July 10 events not as market color but as confirmation that the supplier side has consolidated its pricing power — and plan the next four quarters as if that power will be exercised.