When a Memory Maker Locks a Decade of Raw Wafers: What Micron's $3B GlobalWafers Move Signals for OEM and EMS Sourcing Strategy Through 2027

Micron's July 9 announcement — up to $3 billion to strengthen the U.S. semiconductor ecosystem, $500M in strategic financing for GlobalWafers' Sherman, Texas 300mm plant, and a ten-year raw silicon wafer supply agreement — is being read by markets as a stock story. For sourcing organizations, the more durable signal sits one layer higher in the chain: the bottleneck is migrating from fab capacity to substrate supply, and it is being regionalized.

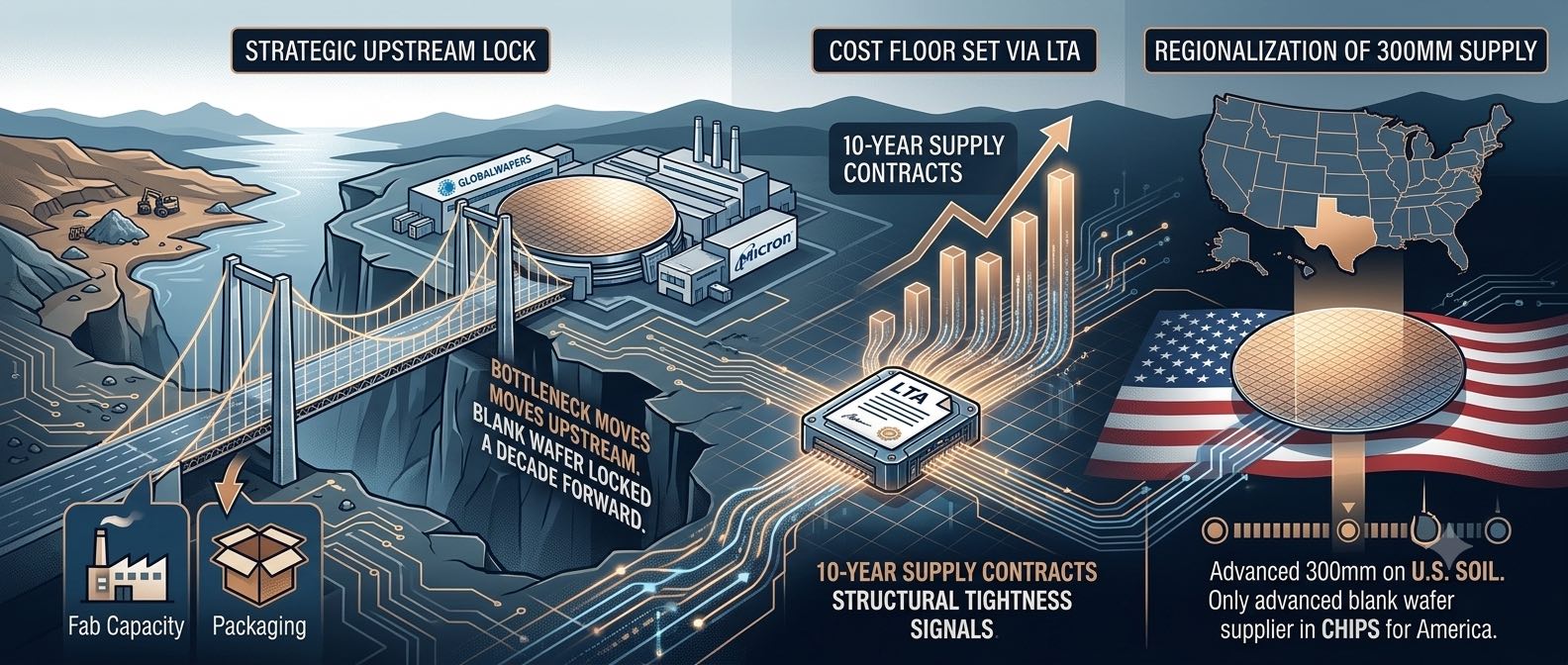

On July 9, 2026, Micron announced it would invest up to $3 billion to strengthen the U.S. semiconductor supply-chain ecosystem, with the centerpiece being $500 million in strategic financing directed at GlobalWafers America's 300mm raw silicon wafer manufacturing facility in Sherman, Texas, alongside a ten-year supply agreement that secures a substantial volume of raw wafer capacity for Micron's long-term manufacturing needs. The equity market treated it as a catalyst — Micron shares climbed on the day and GlobalFoundries rose in sympathy — but for procurement and supply-chain organizations, the price action is the least interesting part of the story. What matters is where in the value chain the commitment sits, and what it implies about the shape of memory supply over the next several years.

The raw silicon wafer is the blank substrate at the very top of the semiconductor value chain: an unprocessed 300mm disc that has not yet seen lithography, doping, or metallization. It is the input from which every subsequent step of memory manufacturing proceeds. For two years the industry conversation about supply constraints has centered on fab capacity, advanced-node availability, and back-end packaging congestion — the parts of the chain closest to the finished die. Micron's decision to underwrite substrate capacity a full decade forward relocates the anxiety upstream. The implicit message is that a memory maker of Micron's scale no longer regards raw wafer availability as a commodity input it can source flexibly on demand, but as a strategic constraint worth capitalizing and contracting against for ten years. When a major producer takes that view, sourcing teams downstream should update their own assumptions accordingly, because the cost floor for finished memory is being set by decisions like this one, not by quarterly spot fluctuations.

There is a second dimension that OEM and EMS buyers cannot afford to overlook: regionalization. GlobalWafers is described as the only raw silicon wafer supplier participating in the CHIPS for America Program that is currently capable of locally producing advanced 300mm wafers in the United States. By anchoring its long-term substrate supply to a domestic source under a federal program, Micron is not simply securing volume — it is aligning a critical input with a specific geographic and policy bloc. For any sourcing organization whose bill of materials mixes U.S.-origin memory with manufacturing or delivery footprints in China and the rest of Asia, this is a concrete data point in favor of dual-sourcing and geographic diversification of the memory line. The era in which a buyer could treat "the memory market" as a single global pool with fungible supply is closing; increasingly, where a part is made and under which policy regime determines both its availability and its exposure to trade friction.

The knock-on effects extend beyond memory. Three-hundred-millimeter raw wafers are not a memory-only input; logic, power, and analog manufacturers draw from the same substrate pool. The fact that GlobalFoundries rose on the same announcement is a market acknowledgment that substrate tightening is a shared constraint. Sourcing teams already contending with extended lead times on power devices and automotive-grade components should not read the Micron move as a memory-specific event that leaves their categories untouched. If a leading memory maker judged it necessary to lock a decade of substrate supply, the rational inference is that raw wafer availability will remain a competitive pressure point across multiple device categories, and that lead-time relief in the constrained segments is unlikely to arrive from the supply side in the near term.

Practically, the response for a sourcing organization is to add a layer to how it models memory supply risk. Historically the useful indicators were fab utilization rates, contract-versus-spot price spreads, and back-end lead times. To those, buyers should now add upstream substrate indicators: raw silicon wafer lead times, the share of wafer capacity committed under long-term agreements, and the geographic distribution of qualified 300mm wafer sources. When the top of the chain is increasingly spoken for under decade-long contracts, the residual flexibility available to buyers without such agreements narrows, and that residual is precisely where cost volatility concentrates. Organizations that build substrate visibility into their planning now — and that use long-term agreements, buffer inventory, or qualified secondary channels deliberately rather than reactively — will be better positioned than those still treating raw wafers as an abstraction several steps removed from their purchase orders.

The Micron–GlobalWafers agreement is, in the end, a statement about time horizons. A ten-year contract for a blank wafer is a bet that the structural forces tightening memory supply — AI infrastructure demand, capacity discipline among makers, and the strategic value of domestic manufacturing — will persist well into the second half of the decade. Sourcing teams do not have to share every element of that thesis to act on its implications. It is enough to recognize that the parties closest to the constraint are behaving as though tightness is durable, and to plan procurement, inventory, and supplier qualification around a supply environment that is unlikely to loosen on its own timetable.