When a Hyperscaler Chooses to Recycle DDR4 Instead of Buying DDR5: What Meta's Vistara CXL ASIC Signals for OEM and EMS Memory Sourcing

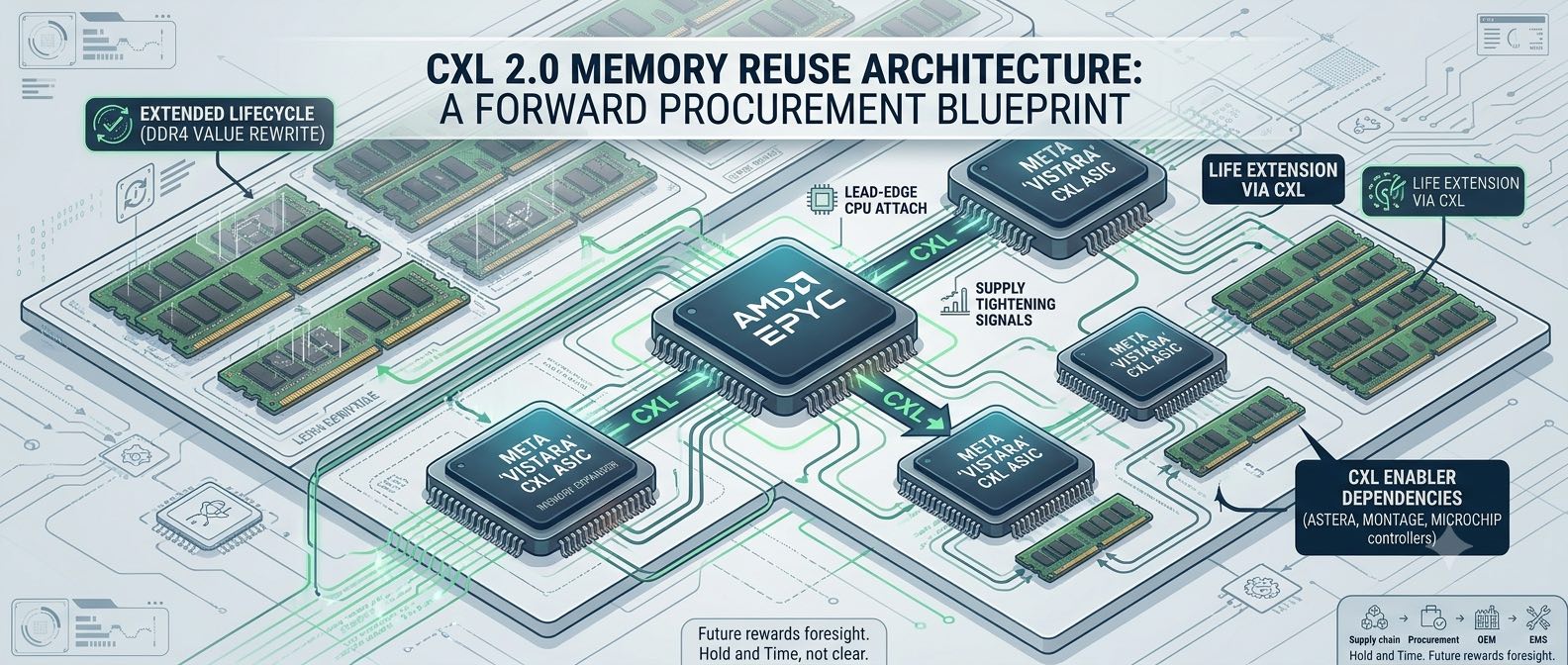

At ISCA 2026, Meta disclosed Vistara, a first-generation custom CXL 2.0 memory-expander ASIC that attaches legacy DDR4-2400 to DDR5-only AMD EPYC servers at production scale. Beneath the engineering headline sits a structural sourcing signal for OEM and EMS procurement teams.

The disclosure is specific and worth stating precisely. At ISCA 2026, held on June 29–30, 2026, Meta presented Vistara, its first-generation custom CXL 2.0 Type-3 memory-expander ASIC. Implemented over a PCIe 5.0 x16 interface, it bridges standard DDR4-2400 RDIMMs to AMD EPYC "Turin" hosts that natively support only DDR5. In Meta's reference configuration, each server pairs 768 GB of local DDR5-6400 with 256 GB of CXL-attached DDR4-2400, reaching 1 TB of total capacity. The deployment is production-scale across millions of servers, and for certain disaggregated inference workloads it reduces required server counts by as much as 25%.

The stated motivation is unambiguous: with DDR5 pricing elevated through the current memory shortage, Meta is engineering its way around what its peers have started calling the memory tax. For procurement leaders, the interesting question is not whether Meta saves money — it plainly does — but what the decision reveals about the shape of the memory market OEM and EMS teams will be buying into for the rest of 2026.

The first read-through concerns the residual value of legacy DRAM. Under normal lifecycle logic, DDR4 is a declining asset: as it approaches end-of-life, its value should erode and its relevance should fade. The past year has inverted that expectation, with some legacy DDR4 configurations posting quarter-on-quarter increases in the range of 50% — context that predates this week and should be treated as continuity, not a fresh signal. What Vistara adds is confirmation from an unusually credible source. When an operator that optimizes cost to the last dollar commits custom silicon and a fleet-wide rollout specifically to extend the working life of memory that was scheduled for retirement, that is a de facto appraisal. Sourcing teams carrying DDR4 in active or transitional bills of materials should recalibrate the floor under those parts upward, not downward, and should be cautious about last-time-buy math that assumes a conventional EOL decay curve.

The second read-through is less obvious and, for buyers, more consequential. A meaningful share of secondary-market DDR4 supply has historically originated from hyperscaler decommissioning — the refresh cycle that pushes retired modules into the open channel where OEM and EMS teams, and the traders who serve them, can source them. Vistara points in the opposite direction. If keep-and-reuse via CXL becomes a repeatable pattern across large operators, the volume flowing from decommissioning into the secondary channel contracts. The paradox is worth internalizing: a technology designed to prolong the life of legacy memory can, in the near term, make that same memory harder to source on the open market. Teams that rely on the secondary channel for DDR4 continuity should factor in the possibility that this supply lane narrows precisely as demand for legacy density holds firm.

The third read-through moves the lens from the memory to the enabler. Vistara is Meta's own design, but the broader architecture it validates — CXL Type-3 memory expansion as a mainstream cost lever — is served by merchant controllers from suppliers such as Astera Labs, Montage Technology, and Microchip. As reference designs and hyperscaler practice normalize memory disaggregation, the demand curve for CXL expander controllers steepens, and those parts move from a specialist line item toward a planning consideration for any platform team weighing memory cost against capacity. This does not warrant speculative inventory, but it does warrant adding the family to the watchlist and understanding lead-time behavior before it becomes a constraint.

For an OEM or EMS procurement function, the practical posture follows directly. Treat installed and inventoried DDR4 server memory as an asset with a higher floor than a standard EOL model implies, and resist reflexive liquidation. Monitor hyperscaler decommissioning cadence as a leading indicator of secondary DDR4 availability, and secure continuity quantities while the channel remains loose rather than after it tightens. And track the CXL Type-3 expander ecosystem as an emerging dependency, so that a memory-cost strategy built around disaggregation does not later collide with a controller lead-time surprise.

The larger point is that memory sourcing in 2026 is no longer a question of new-part pricing alone. When a hyperscaler builds silicon to reuse what it already owns, it is telling the rest of the market that the lifecycle of a memory part — and the value locked inside idle inventory — has been rewritten. Procurement teams that read the signal early will plan their memory positions around a market that rewards holding, monitoring, and timing far more than it rewards clearing.