Why the Second 2026 Analog and Power Price Hike Matters More Than the First: Reading the ST, Infineon, TI and NXP Cadence for OEM and EMS Sourcing

A cluster of analog and power leaders is putting a second 2026 price increase into effect within a single week, and the cadence — not the 5%–15% headline — is the real story for procurement teams. This piece reads the signal behind back-to-back hikes from ST, Infineon, TI and NXP, and what OEM and EMS buyers should institutionalize before pricing power settles permanently on the supply side.

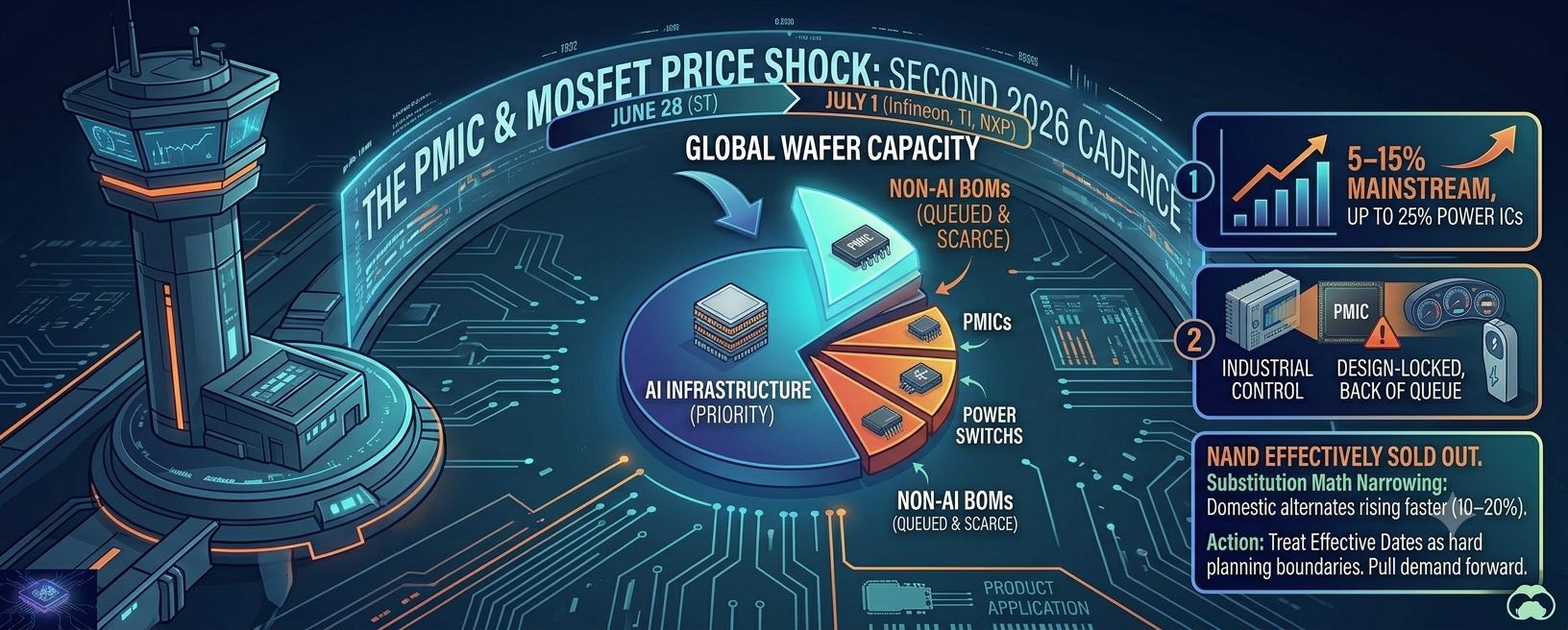

When a single vendor raises prices, procurement treats it as a line-item problem. When four of the largest analog and power suppliers in the world put a second increase of the year into effect inside the same week, the right response is structural rather than tactical. STMicroelectronics has notified customers of an adjustment effective June 28, while Infineon, Texas Instruments and NXP land their increases on July 1 — each described explicitly as the second move of 2026, following adjustments that took effect around April. Mainstream parts are expected to rise in the 5%–15% range, with reports of power switches and ICs at the high end reaching as much as 25%. Domestic Chinese suppliers are tracking the move, with MacMic raising IGBT prices roughly 10% and JieJie preparing 10%–20% increases on MOSFETs and IGBTs.

The percentage is the least interesting part of this. What buyers should focus on is the cadence. A single annual increase can be absorbed into standard cost-down negotiation and quarterly re-pricing; a second increase in the same quarter, from the same vendors, signals that the suppliers read end demand as firm enough to raise twice without losing volume. That is a different market from the one most BOM cost models were built around. The stated rationale — inflation, raw materials, transportation, labor, and in Infineon's case explicitly geopolitical cost pressure — matters less than the underlying confidence the move reveals: in power conversion and power management especially, AI infrastructure has shifted pricing power decisively from the buyer to the seller, and the second hike is the supplier testing how far that shift extends.

The components at the center of this are not specialty parts that a clever redesign can engineer around. TI named PMICs and MOSFETs specifically — the high-volume, general-purpose power building blocks that populate AI server boards, industrial power rails, automotive systems and consumer power supplies alike. Infineon's increases concentrate in power switches and power ICs, the parts feeding EV, automotive and energy-storage demand. ST's language about adding "products not included in the previous increase" tells you the sweep is becoming comprehensive rather than selective. For an OEM or EMS buyer, this means the increase cannot be quarantined to a few exotic line items; it touches the cost base broadly, and the room to offset it through substitution is narrowing as the domestic alternates raise prices in parallel — and frequently by more.

What should procurement institutionalize, rather than merely react to? First, treat effective dates as hard planning boundaries. The difference between an order booked before June 28 or July 1 and one placed the following week is real money at volume, and forecasting discipline that pulls firm demand forward ahead of an announced effective date is no longer opportunistic — it is basic hygiene in a two-hikes-per-quarter environment. Second, re-baseline the substitution math. A spread table built three months ago is stale the moment the majors move 5%–15% and the alternates move 10%–20%; some second-source cases that looked attractive in Q1 no longer clear the threshold, while others improve, and only a fresh calculation tells you which. Third, read NCNR and allocation terms with fresh scrutiny. In a repricing environment, suppliers and distributors lean harder on non-cancellable commitments and tighter allocation, and locking a price in exchange for a non-cancellable position at an elevated level is a trade that needs an explicit exit thesis, not a reflex.

There is also a channel dimension that disciplined buyers can use. Maker announcements do not reach spot and secondary pricing instantly; distributors first absorb the new sheet against in-transit and booked orders, and real spot quotes typically reset two to three weeks afterward. That lag is a genuine planning window. Buyers with visibility into old-price inventory — their own or a trusted channel partner's — have a short interval in which the spread between the legacy cost basis and the post-hike level is at its widest, and the teams that map that inventory ahead of time convert the lag into margin rather than scrambling after the sheets turn over.

The strategic read is straightforward. The 5%–15% will be re-negotiated, absorbed and largely forgotten within a couple of quarters. The cadence will not. Two coordinated increases in one quarter from the analog and power majors is the market telling procurement that the era of assuming power and analog pricing drifts gently downward is over for now. The organizations that respond by building forecasting discipline, live substitution models and channel visibility into standing process — rather than treating each notice as a one-off fire drill — are the ones that will carry a structurally lower cost base into 2027.