TSMC's June 24 All-Node Price Hike Is Less About the Leading Edge and More About Mature Capacity: What OEM and EMS Sourcing Teams Should Read From It

TSMC notified customers on June 24 of a 5–10% price increase spanning every advanced node from 7nm down, covering roughly three-quarters of its wafer revenue. For OEM and EMS buyers the immediate cost impact is real but slow-moving; the more consequential signal is the resource reallocation away from mature nodes, which reshapes lead times and availability across the legacy parts that dominate most bills of materials.

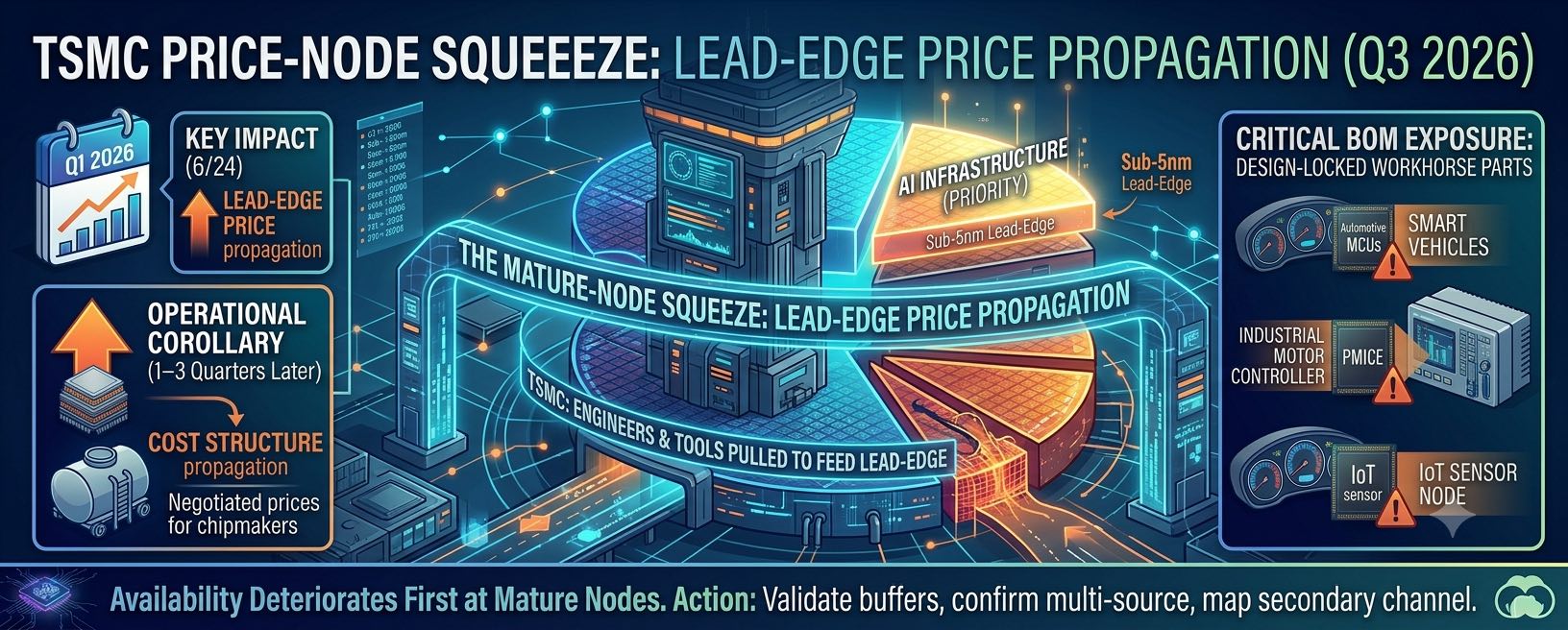

On June 24, 2026, TSMC notified its customers of a broad wafer-foundry price increase of 5–10% across every advanced node at 7nm and below — not only the newest N2 and N3 processes but the mature leading-edge nodes N4, N5 and N7 that have anchored its output for years. By the foundry's own framing the move touches the processes that generate roughly three-quarters of its wafer revenue, which makes this less a targeted adjustment than a system-wide repricing of advanced manufacturing. For procurement organizations, the instinct is to treat this as another line item in an already inflationary year. That instinct is correct but incomplete, because the headline number and the operational signal sit in two different places.

The drivers behind the hike are by now familiar, and worth stating plainly so the conclusion isn't mistaken for novelty. AI and high-performance computing have absorbed leading-edge capacity faster than it can be built; N2 entered volume production only at the very end of 2025 and is already reported as booked through the end of 2026; capital expenditure and EUV-driven process complexity continue to push unit economics upward. In a sold-out market, pricing power flows to the supplier, and the customers most exposed — NVIDIA, AMD, Apple, Qualcomm, MediaTek — are precisely those whose roadmaps are locked to the most advanced nodes. None of this is in dispute, and none of it is, on its own, new information for a sourcing team that has been tracking the four-year hike cadence TSMC signaled in late 2025.

What deserves closer reading is where the cost actually lands and over what horizon. A wafer-price increase at the leading edge does not arrive on an OEM's doorstep as a spot-market shock; it propagates through the finished-device cost structure of the chipmakers who buy those wafers, and it surfaces in negotiated component pricing one to three quarters later. For a buyer sourcing a current-generation GPU, accelerator or flagship SoC, the relevant planning response is to revisit cost models and contract terms with the expectation that advanced-node silicon will carry structurally higher pricing for several years, not to expect an overnight jump. Treating the leading-edge hike as an emergency tends to misallocate attention toward the parts of the BOM where buyers have the least leverage and the least substitutability.

The more actionable signal is the corollary that has accompanied this hike in the reporting: to feed sub-5nm demand, TSMC has been shifting equipment and engineering resources away from mature nodes, with the consequence that mature-process capacity is tightening for customers who are not on the priority list. This is the part of the story that reaches deep into a typical bill of materials, because the components built on 28, 40, 55 and 65nm processes — automotive and industrial microcontrollers, power-management ICs, a broad tail of analog and interface devices, sensor front-ends — are exactly the parts that most products depend on in volume and can least afford to lose. When a foundry reallocates toward its highest-margin work, the parts that slip are not the marquee chips but the unglamorous, high-runner components whose absence stops a line.

For OEM and EMS sourcing teams, the practical implication is to widen the lens beyond the headline. Lead-time monitoring should be focused on mature-node-heavy categories rather than on the leading-edge devices that dominate the news, because that is where availability is most likely to deteriorate first and where the early indicators — lengthening quoted lead times, tighter allocation, increased selectivity on date codes and lot traceability — will appear. Where a product line carries known mature-node dependencies, this is the moment to validate buffer positions, confirm multi-source qualification status, and treat the secondary and spot channels not as a last resort but as a planned-for relief valve for the components most exposed to reallocation. The teams that come through the next several quarters in the best shape will be the ones that read this hike correctly: not as a leading-edge price event to absorb, but as confirmation of a structural mature-node squeeze to position against.