Power Semiconductors Become the Second Front of the 2026 Pricing Wave: Reading Infineon's July 1 Hike for OEM and EMS Sourcing Strategy

For most of the first half of 2026, the procurement conversation lived inside memory — DRAM and NAND allocation, HBM4E samples, DDR5 contract resets. Power semiconductors moved more quietly, but they are now unmistakably the second front of the pricing wave, and the fundamentals beneath them are arguably more durable than the memory cycle. This briefing reads Infineon's July 1 second hike, ST's repricing, and the 52-week SiC bottleneck as a single strategic signal for OEM and EMS buyers.

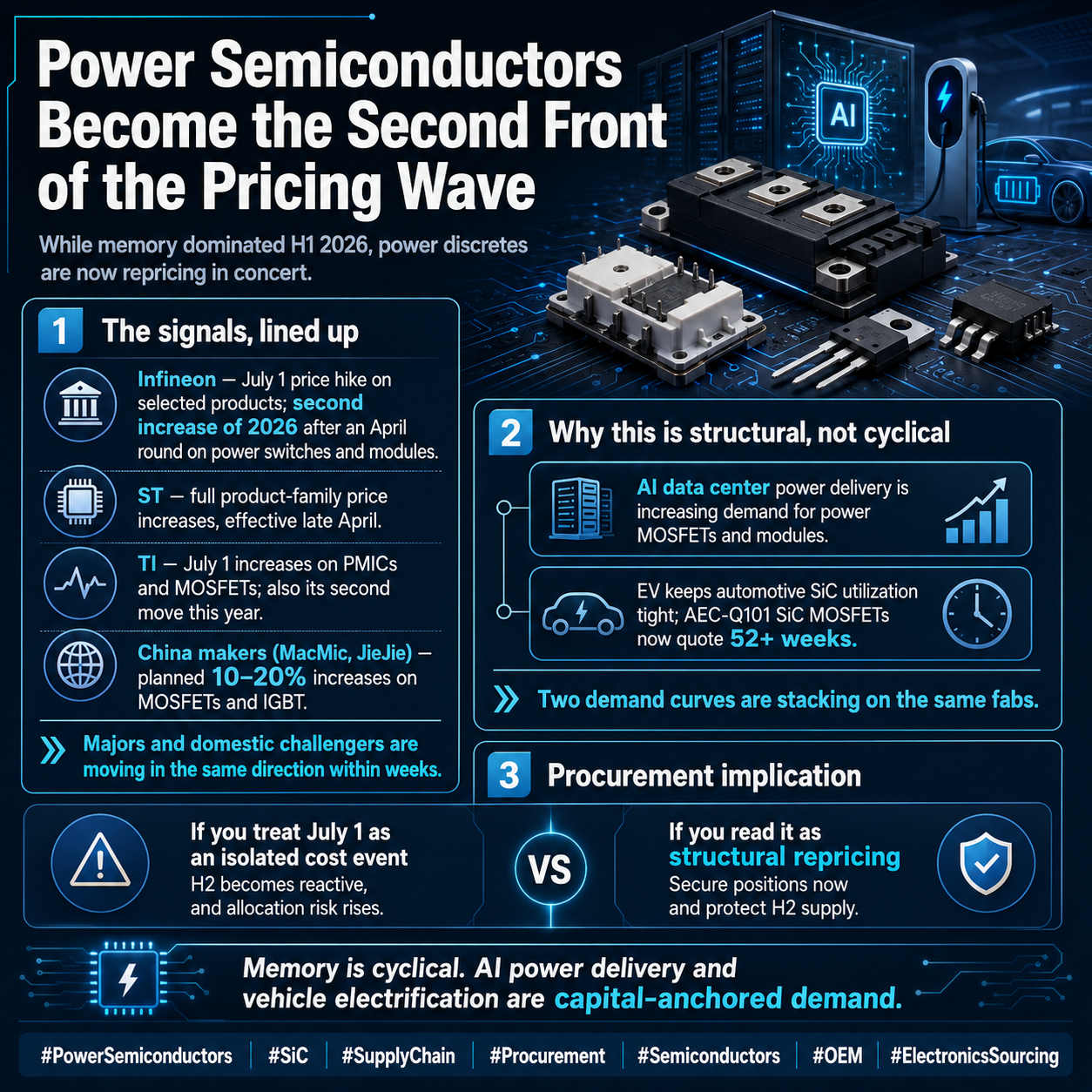

When Infineon notified customers on May 26 that prices on selected products would rise effective July 1, it framed the move in the language the industry has heard all year — rising supply-chain costs, energy, raw materials, transportation, and demand running ahead of expectations. What deserves attention is not the language but the cadence. This is Infineon's second adjustment of 2026, following an April round that lifted power switches, power modules, and related ICs by a reported 10% to 25%. Two price actions on power product lines inside a single half-year is not a cost pass-through; it is a supplier telling the market that the structural floor under power semiconductors has moved, and that buyers should plan their 2026 H2 budgets around a higher baseline rather than a temporary spike.

The move does not stand alone, which is precisely why it matters for sourcing strategy. ST notified customers in March of increases across multiple product families, with new pricing effective around late April, and Texas Instruments is set to raise prices on July 1 covering PMICs and MOSFETs — also its second round of the year. Beneath the majors, Chinese suppliers including MacMic and Jiangsu JieJie Microelectronics are planning 10% to 20% increases on MOSFET and IGBT lines. When the franchise leaders and the domestic challengers move in the same direction within weeks of one another, a buyer can no longer treat any single notice as negotiable noise; the entire power-discrete and power-module category is repricing in concert, and the negotiating leverage that an OEM might normally hold against one supplier evaporates when every alternative source is moving the same way.

The demand picture explains why this is structural rather than cyclical, and it is the part procurement teams should internalize before they finalize 2026 H2 commitments. Two independent demand curves are stacking onto the same silicon and the same fabs at once. AI data center power delivery — server power supplies, rack-level distribution, the entire conversion layer that feeds accelerator boards — runs on power MOSFETs and power modules, and the build-out of AI infrastructure has pulled that demand far above what most suppliers planned capacity for even a year ago. At the same time, electric-vehicle demand keeps automotive SiC pinned against its ceiling. Automotive-qualified SiC MOSFETs are now quoted at 52 weeks or longer across multiple procurement channels, and AEC-Q101 qualified SiC has become the single most constrained category in the entire power market — a function of limited wafer supply, long and unforgiving qualification cycles, and EV volumes that show no sign of easing. Unlike a memory cycle, which inflates and deflates with inventory corrections, these two demand sources are tied to multi-year capital programs that do not reverse on a quarterly basis.

For OEM and EMS buyers, the strategic implication is that the window for proactive action is open now and narrowing. The first move is to re-baseline 2026 H2 cost models against the higher post-July floor rather than against H1 pricing, because any BOM costed on April numbers will be wrong by the time it reaches the floor. The second is to separate the genuinely constrained categories — automotive SiC above all — from the merely repricing ones, and to treat a 52-week franchise lead time as a signal that the authorized channel cannot serve urgent demand at all, which means qualified secondary and spot sourcing must be planned into the supply strategy rather than improvised during a line-down event. The third is to read PCN frequency as a leading indicator: as PCNs cluster and lead times on mature part numbers extend, the category tends to migrate from pricing pressure toward allocation and eventually toward end-of-life, the same sequence memory has already walked through this year.

The broader read is that power semiconductors are now following the trajectory memory traced over the past several quarters, but from a more durable demand base. Memory is a cycle; AI power delivery and vehicle electrification are structural, capital-anchored demand that does not unwind with an inventory correction. Buyers who treat the July 1 hike as an isolated cost event will spend the second half of 2026 reacting to allocation; buyers who read it as the opening of a structural repricing will use the next several weeks to secure positions, qualify alternates, and lock the inventory that becomes leverage once the rest of the market turns its attention from memory to power.