The Other NAND Crisis: Why SLC, MLC, and Low-Density eMMC Are Disappearing Faster Than the AI Memory Boom Suggests

While the industry watches enterprise NAND allocation battles, a quieter crisis is unfolding at the opposite end of the density spectrum. SLC NAND shortages have triggered panic stockpiling, MLC contract prices doubled in Q1 2026 with another doubling possible in Q2, and low-density eMMC supply is breaking down as major manufacturers exit legacy nodes. This analysis examines the structural drivers and what they mean for OEM and EMS sourcing strategy.

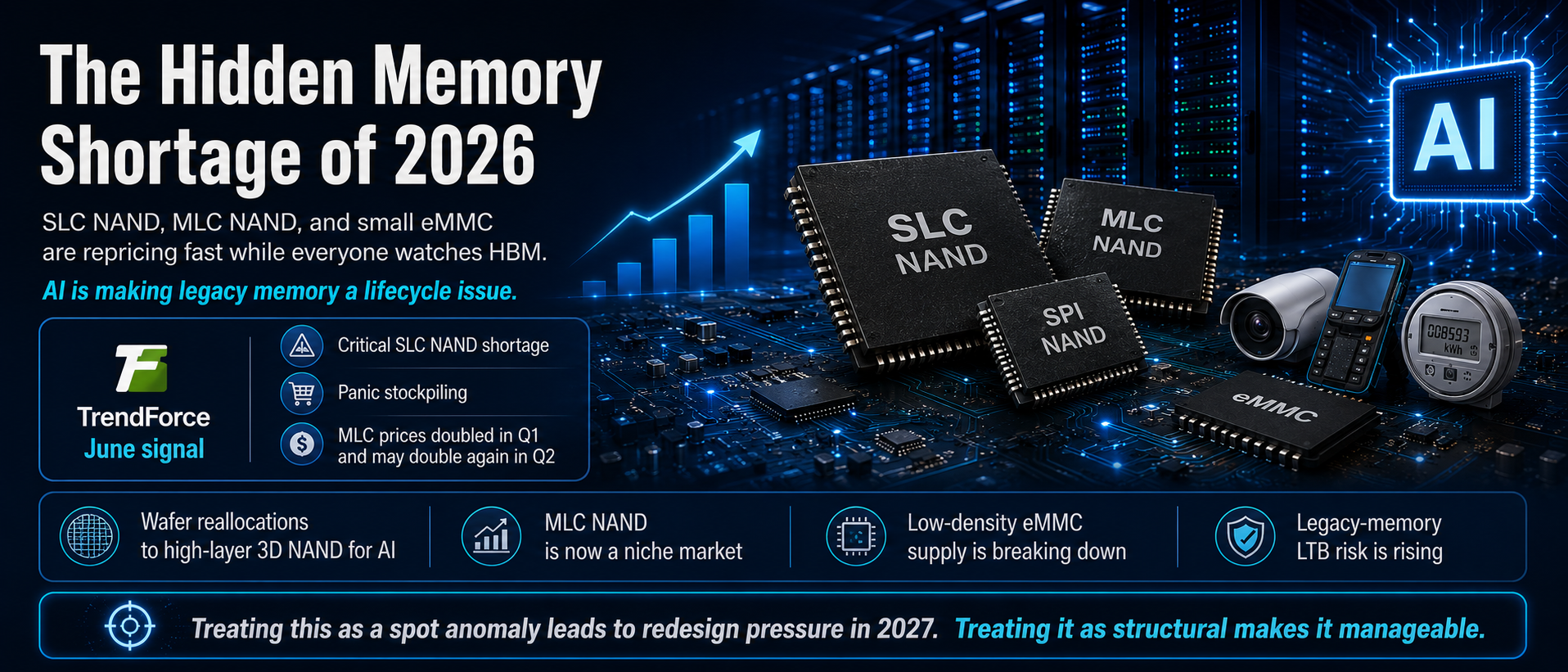

The semiconductor industry has spent the first half of 2026 transfixed by the AI memory supercycle — HBM allocation, DDR5 contract resets, enterprise SSD sell-outs. Yet the most acute supply failure of the second quarter is happening where almost nobody is looking: at the bottom of the NAND density curve. According to TrendForce's June assessment, a critical shortage of SLC NAND has sparked panic stockpiling and price increases of a magnitude rarely seen in this segment, while MLC inventories are effectively depleted. DigiTimes reported in March that MLC contract prices had already doubled in the first quarter and could double again in the second — a trajectory that would make legacy NAND, not HBM, the fastest-appreciating memory asset of 2026.

The mechanism behind this squeeze is straightforward but irreversible in the medium term. Samsung, Kioxia, SanDisk, and Micron have spent the past several quarters reallocating wafer capacity toward high-layer 3D NAND destined for AI servers and enterprise SSDs, where contribution margins are multiples of what legacy parts can deliver. TrendForce formalized the consequence in January: with the majors exiting, MLC NAND has transitioned to a niche market. The exit is not a temporary production cut that recovers when pricing improves — the tooling, engineering attention, and fab floor space are being permanently repurposed. At the same time, demand for small-density storage is rising rather than falling, as AI edge devices — cameras, gateways, industrial sensors with on-device inference — pull in precisely the 4GB-to-8GB eMMC and SLC-class parts that the majors no longer want to make.

What remains of supply is consolidating around a small group of niche specialists, and their behavior tells buyers everything they need to know about the balance of power. Macronix has restarted NT$22 billion in capital expenditure to expand MLC eMMC and NOR output — its eMMC revenue grew 94% quarter-over-quarter and nearly fortyfold year-over-year — and has moved to a monthly repricing model, an arrangement suppliers only impose when they are confident demand cannot walk away. Winbond's capacity is booked through 2027. GigaDevice has guided publicly that niche DRAM and NAND pricing will continue rising through the end of the year. These companies are absorbing demand, but their combined wafer base cannot replace what the majors abandoned; full utilization at every niche fab still leaves a structural deficit.

For OEM and EMS procurement organizations, the implications run deeper than price. The first is lifecycle risk: any long-lifecycle product — industrial controllers, medical devices, metering, automotive infotainment platforms — carrying raw SLC NAND, SPI NAND, or low-density eMMC now faces a meaningful probability of a last-time-buy event within the next twelve months, and legacy-node LTB windows historically open once and briefly. Procurement teams should be running BOM-level exposure audits now, while requalification options still exist, rather than after a PCN forces the issue. The second is contract structure: against suppliers repricing monthly, conventional quarterly pricing agreements transfer all timing risk to the buyer. Shorter validity windows, indexed pricing clauses, and earlier volume commitments are the rational responses, however uncomfortable. The third is channel integrity: every steep price rally in a legacy segment draws remarked, refurbished, and pulled parts into the open market, and incoming inspection rigor — date-code verification, traceability documentation, periodic decap sampling on critical parts — becomes a cost of doing business rather than an optional control.

The strategic reading is that the AI buildout is not merely consuming advanced memory capacity; it is deleting the economic rationale for legacy capacity altogether. Phison's CEO has described NAND prices doubling within six months and at least one foundry demanding three years of payment in advance — conditions that signal a seller's market extending well beyond the AI segments that created it. Buyers who treat the SLC/MLC/eMMC squeeze as a temporary spot anomaly will find themselves redesigning boards under time pressure in 2027. Those who treat it as the structural endpoint of legacy NAND — and act on qualification, contracts, and inventory accordingly — will navigate it as a manageable transition. The window for choosing which group to belong to is closing quarter by quarter.