When the Memory Rally Bifurcates: How OEM and EMS Sourcing Teams Should Read the 3Q26 Split Between AI-Driven and Consumer Demand

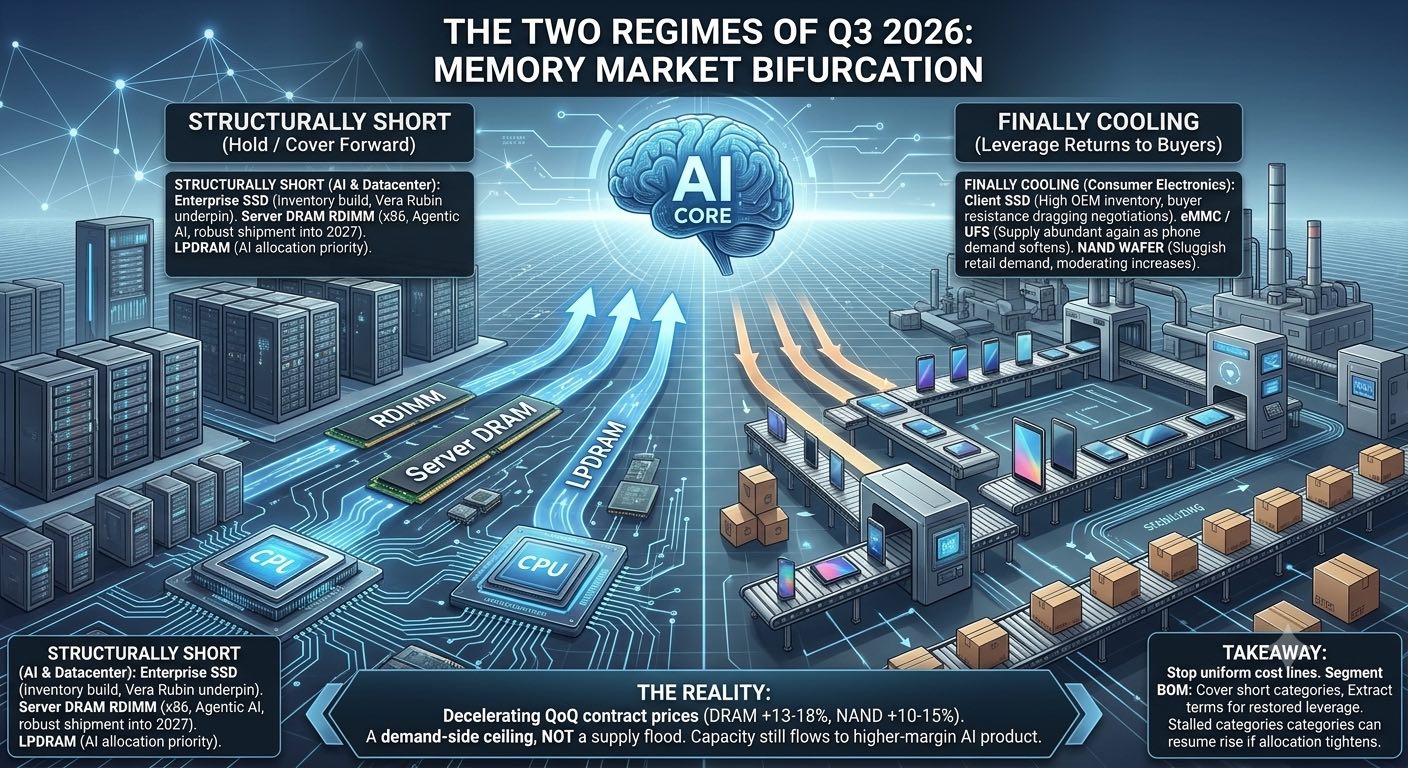

TrendForce's July 3 pricing survey confirmed that 3Q26 memory contract increases are moderating (DRAM +13-18% QoQ, NAND +10-15%), but the more consequential development is structural, not numerical. For the first time this cycle, the market is separating into two demand regimes requiring distinct sourcing playbooks: an AI- and server-driven segment that stays firmly undersupplied, and a consumer-facing segment where buyer affordability has finally capped pricing power.

For roughly a year, memory procurement has operated under an unusually simple rule: prices rose across essentially every category, so the dominant question was how much cost to accept and how far ahead to cover. TrendForce's July 3, 2026 pricing survey signals that this uniform regime is ending. Conventional DRAM contract prices are forecast to rise 13–18% QoQ in the third quarter and NAND Flash 10–15% — both still positive, but decelerating from the record pace of earlier quarters. The number that matters to sourcing teams, however, is not the headline increase; it is the widening gap between two categories of demand that now behave in opposite ways.

On the firm side of the market, the drivers are structural and unlikely to reverse within the planning horizon. Enterprise SSD pricing continues upward even as CPU shortages constrain system shipments, because buyers are choosing to build inventory ahead of complete-system availability rather than wait. Suppliers are actively reallocating capacity toward enterprise SSD, supported by the gradual rollout of NVIDIA's Vera Rubin platform, yet shortages of internally sourced DRAM continue to constrain small-capacity, high-performance drives. Server DRAM remains undersupplied through the quarter, with x86-plus-RDIMM configurations serving as the primary platform for Agentic AI workloads and shipments projected to remain robust into 2027. LPDRAM stays tight because suppliers prioritize AI allocation, and even graphics DRAM — despite a GDDR7 demand wave that never fully materialized around NVIDIA's RTX PRO 6000 Blackwell — holds firm on flexible capacity reallocation.

On the softening side, the change is equally clear and, for sourcing teams managing consumer-oriented product lines, more immediately actionable. Client SSD increases are moderating because PC OEMs built inventory aggressively in the first half, leaving elevated stock and little willingness to absorb another round of price hikes; suppliers have adopted more flexible pricing to protect shipment momentum, and negotiations have lengthened as a result. The eMMC and UFS segment represents the most pronounced reversal: previously among the most constrained categories, supply has become relatively more abundant in the third quarter as smartphone demand weakens and OEMs resist further cost pass-through, eroding supplier pricing power and narrowing increases. NAND wafer pricing is moderating substantially as retail-facing demand for USB drives and memory cards stays sluggish and module makers keep purchases low, unable to pass elevated upstream cost to end markets.

For OEM and EMS procurement organizations, the operational implication is that a single memory sourcing strategy is no longer adequate. The AI- and server-linked categories — enterprise SSD, server RDIMM, LPDRAM — warrant continued forward coverage and, where feasible, long-term supply agreements that lock volume and smooth pricing; TrendForce explicitly attributes part of the server DRAM moderation to LTA-governed procurement, which is precisely the mechanism that has protected disciplined buyers this cycle. The consumer-facing categories, by contrast, now offer negotiating leverage that did not exist six months ago. Teams sourcing eMMC, UFS, client SSD or wafer for consumer and industrial-adjacent designs should resist accepting opening quotes, use elevated channel inventory as a bargaining position, and avoid over-committing to forward volume in a segment where momentum is fading.

A critical interpretive caution belongs in every procurement review built on this data. The moderation in consumer memory is a demand-side ceiling, not a supply-side flood. Prices are not falling; they have simply reached the limit of what consumer end-markets can absorb, while suppliers continue to withhold capacity from the open market in favor of higher-margin AI and server product. That distinction matters because it defines the risk profile of any timing decision: a category that has stopped rising because buyers are exhausted can resume rising quickly if AI allocation tightens further or if consumer demand stabilizes. Sourcing teams should therefore treat the current consumer-NAND softening as a tactical window to be used deliberately — to rebalance inventory, renegotiate terms, and clear slow-moving positions — rather than as the beginning of a durable downcycle that justifies deferring coverage on the categories still structurally short.

The broader takeaway for 2026 planning is that the memory market has entered a phase where AI infrastructure demand and traditional consumer demand no longer move together, and procurement strategy has to reflect that divergence explicitly. The organizations best positioned through the second half will be those that segment their memory BOM by demand regime, apply forward coverage and LTAs where structural shortage persists, and extract terms where consumer affordability has restored buyer leverage — rather than continuing to treat memory as the single, uniformly rising cost line it was for most of the past year.

Source: TrendForce, July 3, 2026. https://www.trendforce.com/presscenter/news/20260703-13134.html