When Enterprise SSD Demand Resets the NAND Hierarchy: What the 2026 Capacity Reallocation Means for OEM and EMS Storage Sourcing

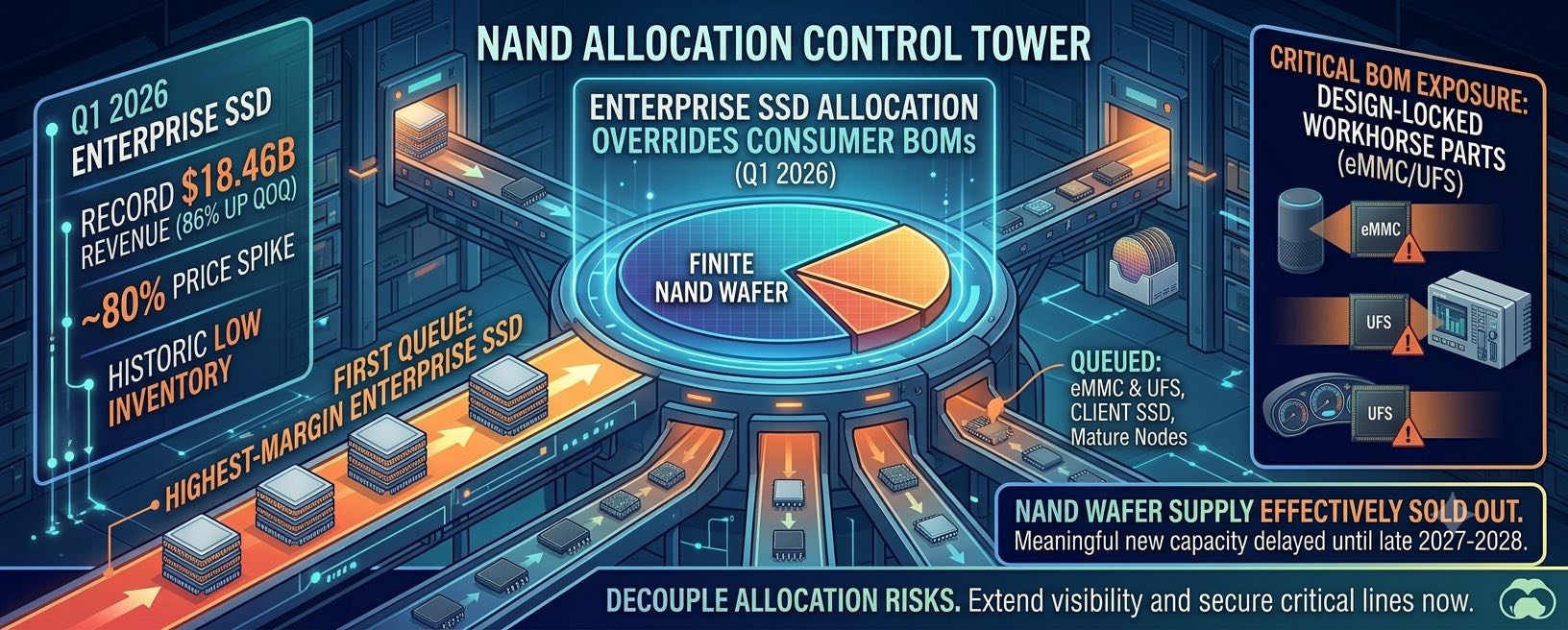

Enterprise SSD revenue reached a record $18.46B in Q1 2026, up 86% QoQ, while contract prices rose roughly 80% in a single quarter and supplier inventories fell to historic lows. As memory makers reallocate wafer capacity toward high-margin AI storage, the pressure is no longer contained to HBM and high-end DRAM — it is now reshaping the availability and cost of general-purpose NAND, client SSDs, eMMC and UFS. This piece examines what the reallocation means structurally for OEM and EMS buyers, and how sourcing strategy should adapt.

For most of the past year, the memory shortage narrative has been written in the language of HBM. The story was clean and compelling: hyperscalers buying AI accelerators, accelerators demanding high-bandwidth memory, and the three large makers tilting their most advanced capacity toward that single, high-value product. What that framing obscured is that the same capital and capacity logic was always going to ripple outward — and in the second quarter of 2026, it has arrived decisively in NAND, with enterprise SSD as the new center of gravity.

The data points are difficult to ignore. Enterprise SSD revenue reached a record $18.46 billion in the first quarter, an 86% sequential increase, driven by the large-scale adoption of generative AI and the storage footprint that AI inference and training workloads require. Contract prices for enterprise drives climbed by approximately 80% in a single quarter, and supplier inventories dropped to levels not seen in years. For buyers who track NAND as a relatively elastic commodity, this is a structural reset rather than a cyclical bump.

The mechanism is straightforward but its consequences are not. Enterprise SSD is the highest-margin destination for finite NAND wafer output, and the major suppliers — Samsung, SK Hynix, Kioxia, Solidigm and SanDisk among them — have every commercial incentive to prioritize it. As capacity shifts toward enterprise-grade products, general-purpose NAND, client SSDs, eMMC and UFS are not removed from the roadmap; they are simply moved down the queue. The same fab that could allocate output to consumer or industrial parts now routes it to enterprise customers locking supply through long-term, cash-for-capacity agreements. The downstream effect is rising prices, lengthening lead times, and a steady migration of general parts into the spot and secondary channel.

This is where the sourcing implications become concrete for OEM and EMS organizations. The components most exposed are not the headline enterprise drives — which most buyers in the industrial and consumer space were never going to secure directly — but the workhorse parts embedded across thousands of BOMs: eMMC and UFS modules in consumer devices, industrial gateways and automotive infotainment, alongside client SSDs and discrete NAND. These are high-volume, design-locked components that cannot be re-specified on short notice, which makes their exposure to allocation both more damaging and harder to mitigate than a one-off enterprise purchase would be.

The supplier roadmap reinforces the direction of travel. Kioxia's 218-layer NAND is ramping at North American customers, and its 245TB QLC enterprise drive is in validation with volume expected in the second half — validation-phase capacity that, predictably, flows to the largest accounts first. SanDisk and WDC have brought QLC enterprise SSDs into volume production into the teeth of a high-capacity QLC shortage. Solidigm is advancing 240-layer NAND, and SK Hynix is already developing 375-layer TLC. Every one of these programs is oriented toward AI storage, and each represents capacity that will not be available to general-purpose parts in the near term.

For procurement leaders, the appropriate response is not to chase enterprise allocation they cannot win, but to institutionalize protection around the general parts they actually depend on. That means extending visibility horizons on eMMC, UFS and client SSD well beyond the usual planning window; converting critical NAND lines to long-term agreements or NCNR buffer stock where supplier terms allow; and treating the secondary channel as a legitimate, monitored sourcing lane rather than an emergency fallback. It also means resisting the temptation to apply DRAM-era assumptions to NAND. The two markets are being drained by different end-products — HBM in one case, enterprise SSD in the other — but the consequence for the parts buried in a BOM is identical: scarcity, cost inflation, and queuing.

The duration of this dynamic matters as much as its severity. NAND is effectively sold out for 2026, and meaningful new capacity is not expected to come online before late 2027 or 2028. That timeline removes any reasonable expectation of near-term relief and turns what might otherwise be a tactical inventory question into a strategic one. Organizations that build their 2026 and early-2027 storage plans around continued tightness — and that secure general-purpose parts before the queue lengthens further — will be materially better positioned than those waiting for a normalization that the supply side has already ruled out.

The headline will continue to belong to HBM and AI accelerators. The risk that quietly accumulates in industrial and consumer BOMs belongs to NAND. Sourcing teams that recognize the difference, and act on the parts they can actually control, will absorb this cycle far better than those still reading last year's script.