When a Single Disclosed Contract Locks a Year of AI-Server MLCC Output: What Samsung Electro-Mechanics' $294M Deal Signals for OEM and EMS Passive Sourcing

Samsung Electro-Mechanics disclosed a one-year, roughly $294M MLCC supply contract with an unnamed US hyperscaler on June 30, with deliveries beginning January 2027. For OEM and EMS procurement teams, the significance is not the headline value but the structural read: high-end passive capacity is now being fenced off through disclosed long-term agreements, and the pressure flows down to the commodity parts most buyers actually carry.

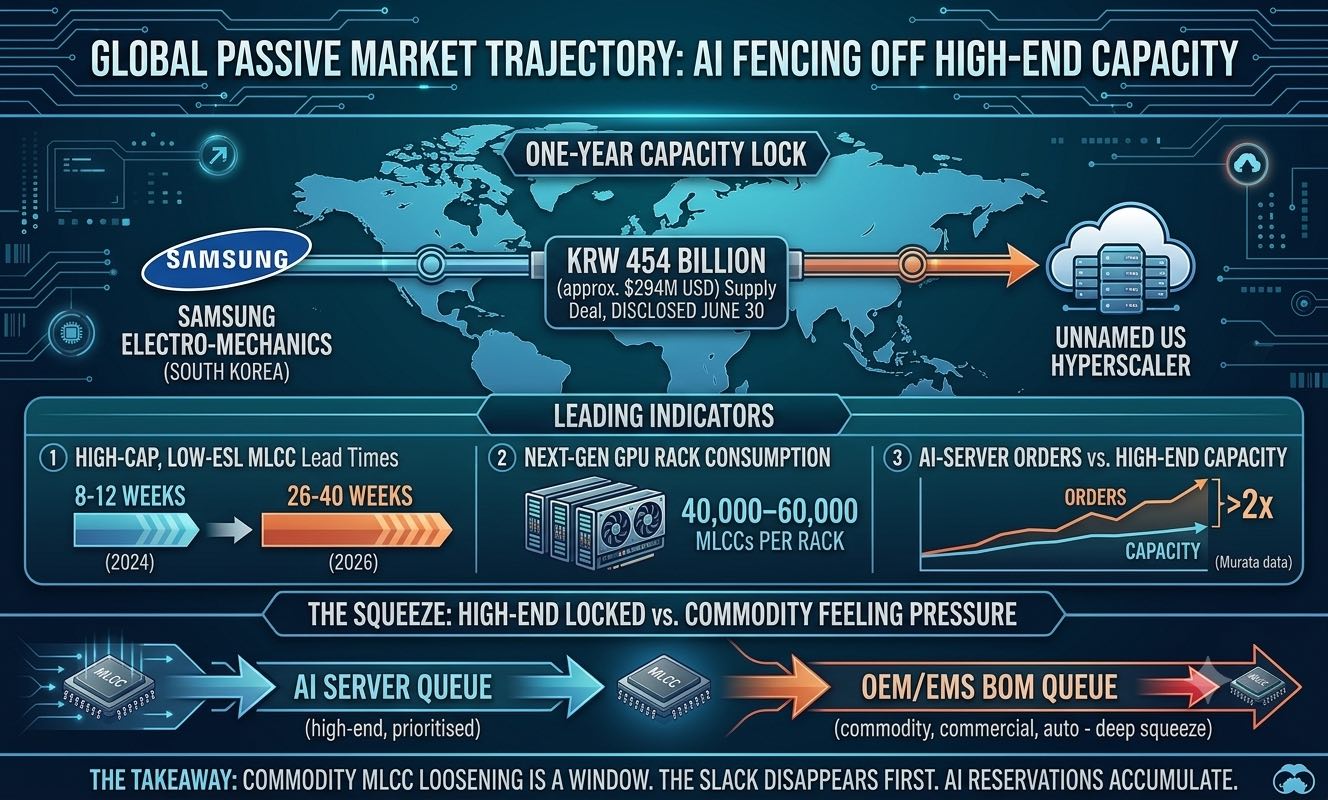

On June 30, 2026, Samsung Electro-Mechanics filed a regulatory disclosure confirming a one-year contract worth KRW 454 billion — roughly $294 million — to supply multilayer ceramic capacitors for AI servers, with shipments commencing on January 1, 2027. The company did not name the customer, but the market consensus points to a leading US hyperscaler, with observers naming Google, AWS and Meta as the plausible candidates. Earlier reports in the final days of June had described the deal as being in final-stage negotiation at around KRW 500 billion; the disclosed figure landed slightly lower at KRW 454 billion, but the substance held.

For procurement teams, the instinct to weigh the headline dollar value misses the point. Against a company that turns over billions of dollars annually across its components, module and substrate businesses, a $294 million single contract is not financially transformative. What makes the disclosure worth a procurement team's attention is what it represents structurally: a top-three global MLCC maker considered a single customer's AI-server demand material enough, and durable enough, to lock through a formal one-year agreement disclosed to regulators. That is a different signal from a spot order or an allocation adjustment. It is capacity being reserved by contract, ahead of delivery, in a segment that was already the tightest in the passive market.

The mechanics of why this matters to broader sourcing are straightforward once the capacity math is laid out. MLCC production capacity — particularly for the high-capacitance, low-ESL parts that AI server power-delivery and decoupling demand — is finite and slow to expand. When a maker signs a high-margin, high-volume AI contract on a long-term basis, it rationally tilts line loading toward that commitment. The parts displaced are not the AI-grade capacitors themselves; they are the general-purpose commercial-grade and, at the margin, automotive-grade MLCCs that OEM and EMS bills of materials depend on in the highest unit volumes. In other words, the visible event concerns a hyperscaler and a premium part, but the downstream consequence lands on the commodity end of the catalogue that most manufacturers never think of as scarce.

The lead-time data already reflects this tilt. High-capacitance, low-ESL MLCCs that quoted 8–12 weeks in late 2024 are now quoting 26–40 weeks in 2026, and high-capacitance parts in the 1206 and 1210 case sizes — the workhorses of power-management stages — have broadly pushed past 20 weeks, with certain codes moving into outright stock-out. The demand driver behind these numbers is difficult to overstate: a single next-generation GPU server rack is estimated to consume 40,000 to 60,000 MLCCs for filtering, decoupling and signal integrity alone. Murata has publicly stated that AI-server MLCC orders currently exceed twice its high-end production capacity, which is the clearest possible admission that even aggressive capacity expansion does not close the gap in the near term. Against that backdrop, a disclosed long-term lock by a competing top-tier maker is best read not in isolation but as one more increment in a sector-wide reservation of scarce capacity.

For OEM and EMS procurement teams, several practical conclusions follow. First, the exposure to watch is not limited to AI-grade parts your own designs may not even use; it is the commercial and automotive high-capacitance codes deeper in the BOM that get squeezed as makers reweight their mix. Second, the loosening seen in some commodity MLCC lead times through the first half of 2026 should be treated as a window rather than a trend — as long-term AI reservations accumulate, that slack is the first thing to disappear. Third, expect NCNR and allocation language to return to distributor terms in parallel with these locks; the ability to source high-capacitance commodity parts today without non-cancellable, non-returnable strings is itself a form of optionality worth using. Fourth, this is a coordinated-behavior sector, not a single-maker story: Murata, Taiyo Yuden and Yageo move on similar cadences, and a disclosed lock by one is a reliable leading indicator that the others' high-end capacity — and by extension the commodity parts that share their lines — will tighten in step.

The measured conclusion is that a $294 million contract does not, by itself, reprice the passive market or create a shortage overnight. What it does is confirm a direction that the lead-time and pricing data have been signaling for several quarters: high-end MLCC capacity is being progressively fenced off through formal, disclosed, long-dated commitments to the largest AI buyers, and the commodity end of the market absorbs the residual pressure. Procurement teams that read the June 30 disclosure as a data point in that trajectory — rather than as an isolated Korean corporate headline — will be the ones positioned to stage the right high-capacitance commodity inventory before the window that exists today has closed.